Revenues and marginal prices — an overview covering all markets

June presented a fascinating and completely directionally driven market picture across the balancing capacity markets in Germany and Austria. Unlike the previous month, both countries acted in complete synchronization this time. We witnessed a massive upward movement across all positive segments, while the negative markets cooled down noticeably across the board. This synchronous dichotomy marks a fundamental difference from May, during which we still observed strong country-specific divergence. A historical look at June 2025 also reveals compelling contrasts. Back then, prices fell almost everywhere, except mFRR+. This year, however, all positive products turned out to be enormous growth drivers.

In the Austrian FCR, the positive trajectory continued. Revenues realized through FlexPowerHub climbed by approx. 8% from around 18.085 €/MW/h to a strong 19.515 €/MW/h.

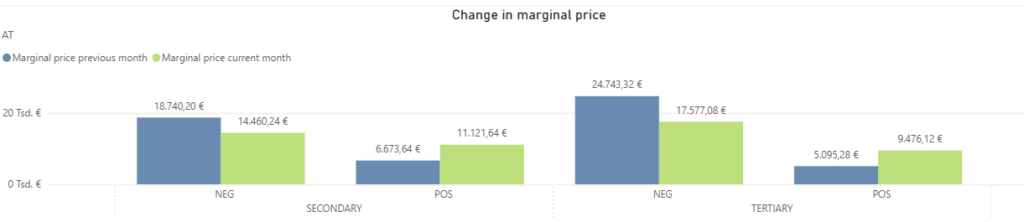

A look at the secondary balancing capacity market reveals the already noted clear divergence in direction. The aFRR+ experienced a massive surge in marginal prices, jumping by around 67% to 11.121 €/MW/h. In a direct year-on-year comparison, this represents a remarkable turnaround, given that this market was still noticeably declining in June 2025. Conversely, the marginal price in the aFRR- cooled down significantly, dropping by approx. 23% from 18.740 €/MW/h to 14.460 €/MW/h.

A mirrored dynamic occurred in the tertiary market. The marginal price for mFRR+ skyrocketed, recording a growth of nearly 86% to 9.476 €/MW/h. In parallel, the mFRR- softened considerably, with marginal prices falling by around 29% to 17.577 €/MW/h.

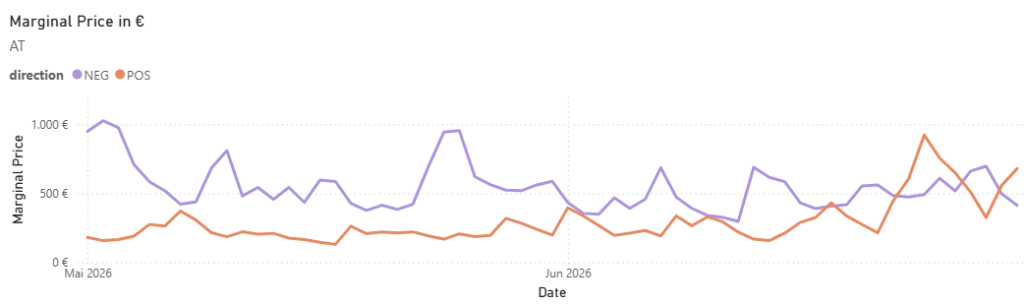

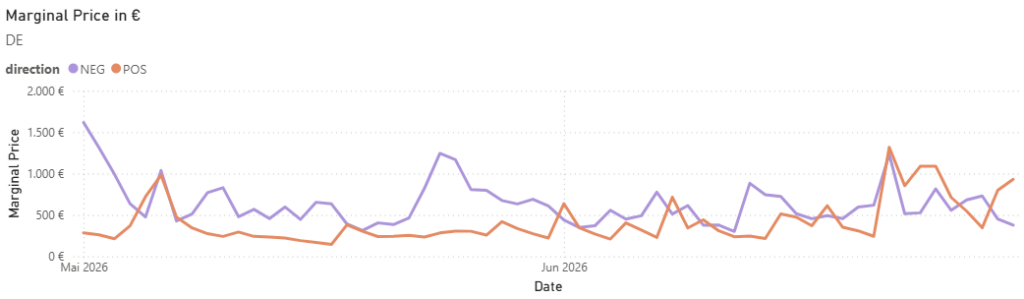

A nearly identical pattern established itself in Germany. Here, too, there was a strict separation between declining negative and rising positive markets.

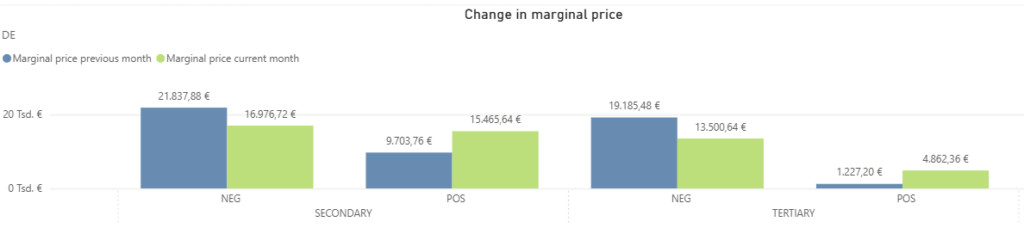

In the aFRR-, marginal prices fell by approx. 22% to 16.976 €/MW/h. The aFRR+, on the other hand, recorded rapid growth, with marginal prices climbing by around 59% from 9.703 €/MW/h to an impressive 15.465 €/MW/h. Such a sharp increase in aFRR+ stands out sharply from June 2025, when the positive market was posting double-digit percentage declines.

In the mFRR, the dynamics were even more extreme than in the neighbouring country. The marginal price in the mFRR+ literally multiplied, catapulting upward with a jump of nearly 300% from a mere 1.227 €/MW/h to 4.862 €/MW/h. At the same time, the mFRR- price decreased by nearly 30% to 13.500 €/MW/h.

The FCR remained completely unfazed by all these sharp fluctuations. Revenues realized through FlexPowerHub held almost steady at the high level of the previous month, reaching 17.379 €/MW/h. This also highlights a striking contrast to June 2025, when FCR revenues had plummeted to a low of under 15.000 €/MW/h.

Comparison of revenues generated with FPH and the market average in the aFRR

In June, the secondary balancing capacity markets (aFRR) in Germany and Austria presented an exceptionally directionally driven development. Revenues and market averages in the positive markets skyrocketed, while the negative markets experienced a noticeable cooldown following the strong previous months. FlexPowerHub adapted to this split market reality highly successfully. Backed by excellent bid acceptance rates, our systems confidently translated the massive gains in the positive markets into financial success, while simultaneously adapting precisely to the altered conditions of the declining markets.

Austria

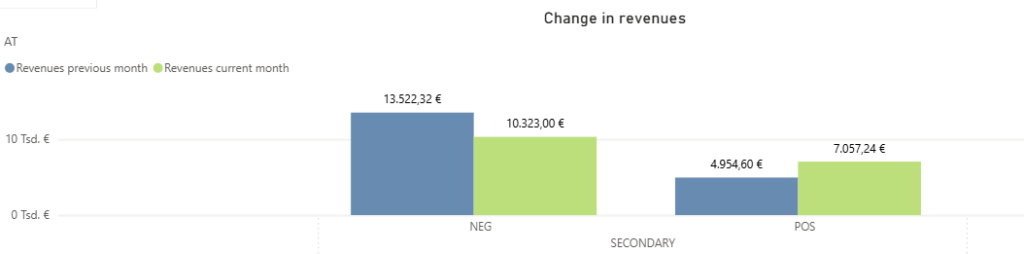

In the aFRR+, June revealed a massive upswing. The market average climbed sharply by approx. 66% from 5.040 €/MW/h in May to 8.377 €/MW/h. FlexPowerHub followed this highly vibrant dynamic very successfully, increasing revenues by around 42% to a remarkable 7.057 €/MW/h. In this rapidly growing environment, our bid acceptance rate remained virtually unchanged at a very high level of nearly 93%. As expected in such an extremely volatile market environment, forecasting performance declined to around 84%. This development marks a fundamental contrast to June 2025, when aFRR+ still recorded a slight drop in revenues alongside a declining market average.

The situation in the aFRR- presented itself in an entirely different way. Following the strong gains of the previous months, the market cooled down noticeably. The market average dropped significantly by approx. 24% to 11.013 €/MW/h. Correspondingly, the revenues generated by our models decreased as well, falling by around 24% to 10.323 €/MW/h. This decline was accompanied by a slightly decreasing bid acceptance rate, which slipped from nearly 95% to around 91%. On a positive note, our forecasting performance improved in this calmer environment, rising to 94% in June. Here too, a historical look back at June 2025 provides an interesting comparison: last year, we were still able to achieve rising revenues, while the market average was slightly declining.

Germany

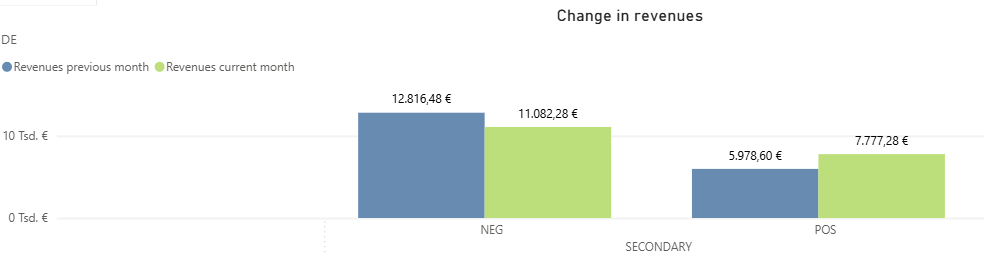

The German balancing capacity market adapted this split pattern even more extremely in the positive market. In the aFRR+, the market average picked up tremendously, jumping by approx. 53% to a remarkable 11.088 €/MW/h. FlexPowerHub utilized this massive potential highly efficiently, simultaneously increasing revenues by around 30% from 5.978 €/MW/h to 7.777 €/MW/h. A particularly pleasing aspect here is the immense consistency of our bid acceptance rate: despite the massive market shifts, it held steady at an outstanding 95%. Although the enormous price fluctuations challenged our forecasting models (leading to a decline in forecasting performance to 70%) a look back at June 2025 reveals a completely new market reality. Last year, revenues in the German aFRR+ segment still decreased slightly instead of exploding in this manner.

The aFRR- mirrored the cooldown seen in Austria. The market average slipped by approx. 23% to 13.076 €/MW/h. Revenues generated by our algorithms followed this downward trend, falling by around 14% from 12.816 €/MW/h to 11.082 €/MW/h. The development of our key performance indicators is highly interesting in this context: the bid acceptance rate recorded an unusually sharp drop to just over 74%. On the flip side, our forecasting models proved highly precise in the market environment, with a forecasting performance climbing significantly from 75% in May to nearly 85% in June. This noticeable correction of revenues in the negative market stands in strong contrast to June 2025, when our revenues grew against the falling market trend and the bid acceptance rate shot up massively.

The June results prove a highly directionally driven market dynamic. FlexPowerHub successfully translated the massive gains in the positive markets into financial success backed by excellent award rates, while expertly adapting its systems to the altered conditions of the negative markets.

Market volatility

June saw a return of selective volatility in the aFRR markets. While May was characterized by widespread calm, the newly awakened dynamic was primarily concentrated in the positive segments of both countries, where the evening decline in solar feed-in triggered price peaks toward the end of the month. In contrast, the negative markets remained remarkably stable and normalized, sustained by increasing storage flexibility, which prevented a recurrence of the extreme price spikes seen the previous year.

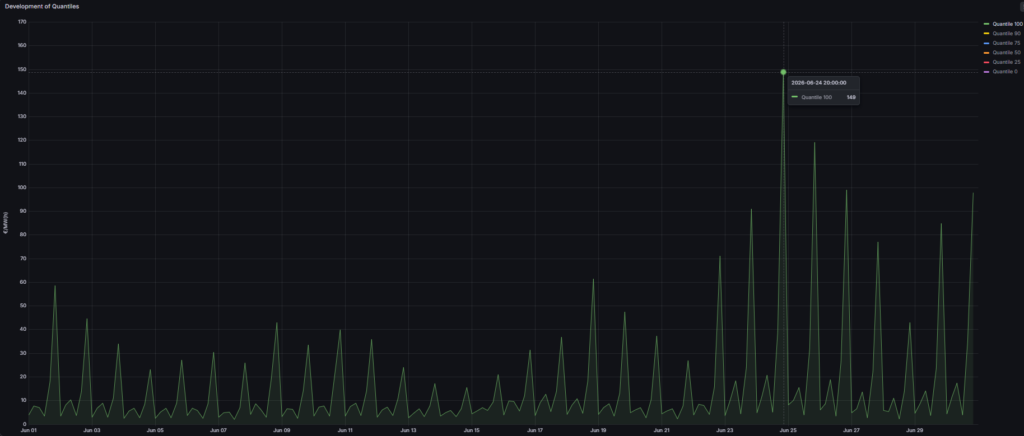

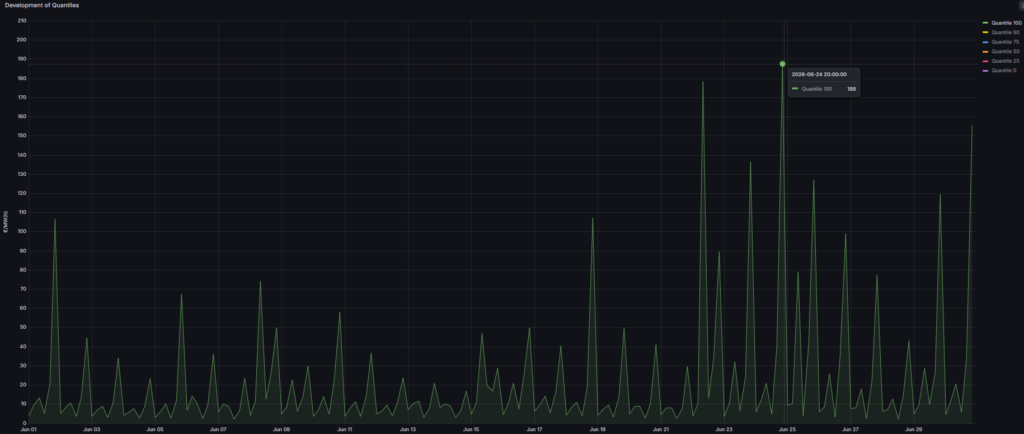

In the Austrian aFRR+,. a striking shift occurred, though it only became noticeable during the final third of the month. The previous month had remained flat and predictable, with a peak value of just under 40 €/MW/h. June also presented a calm picture over long stretches, with prices moving stably below 61.4 €/MW/h for most of the month. It was only toward month-end that volatility picked up noticeably, culminating in a sharp peak of 149 €/MW/h on June 24 at 8:00 PM. This development exceeds the historical peak from June 2025, when the segment marked a high of just 85 €/MW/h. As a result, the final phase of the month in particular demanded a highly agile optimization strategy, whereas the preceding weeks were characterized by a largely relaxed market environment. Even in this increasingly volatile environment, FlexPowerHub maintained outstanding precision, securing an excellent bid acceptance rate of nearly 93%.

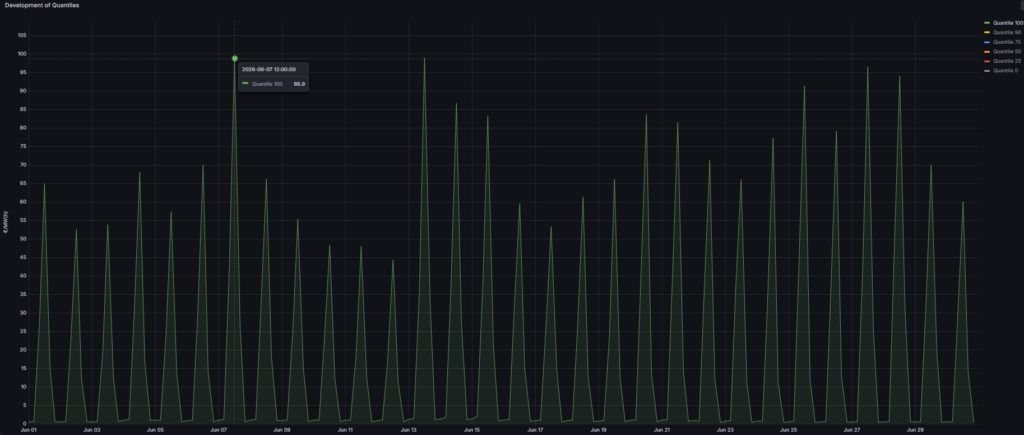

The aFRR- painted an entirely different and far calmer picture.. Here, the maximum price level cooled down even further compared to the already relaxed previous month. While May still saw peaks of 137 €/MW/h, June reached its absolute maximum at a moderate 98,9 €/MW/h, which was recorded twice: on both June 7 and June 13, each time at 12:00 PM. These values, however, did not represent singular, isolated price spikes; rather, the market moved very stably within a narrow corridor between 44,4 €/MW/h and 94,1 €/MW/h throughout the entire month. This reliable characteristic recalls the fundamental pattern of the previous year, when prices likewise moved within a fixed range without genuine outliers. However, the general price level in June 2025 was slightly higher, with prices fluctuating between 68,7 €/MW/h and a peak of 118 €/MW/h back then. Our optimization models took full advantage of this calmer, more stable market structure, proving their immense precision with a strong forecasting performance of 94%.

The German market mirrored the events of its neighbour almost identically in the positive market. In the aFRR+, volatility also picked up noticeably compared to the calm May, with this dynamic characterized by regular fluctuations and occurring at a generally elevated level. Consequently, it was not a single, isolated price outlier when the market reached its peak of 188 €/MW/h on June 24 at the exact same time as in Austria. Despite this increased activity, a look back at the previous year confirms what was actually a very controlled situation: in June 2025, the market was still shaken by a massive spike of 379 €/MW/h. The current development is therefore lively and moving, yet remains far from the extremes of the previous year. Throughout these extensive market shifts, FlexPowerHub demonstrated immense consistency in bidding precision, maintaining an outstanding bid acceptance rate of 95%.

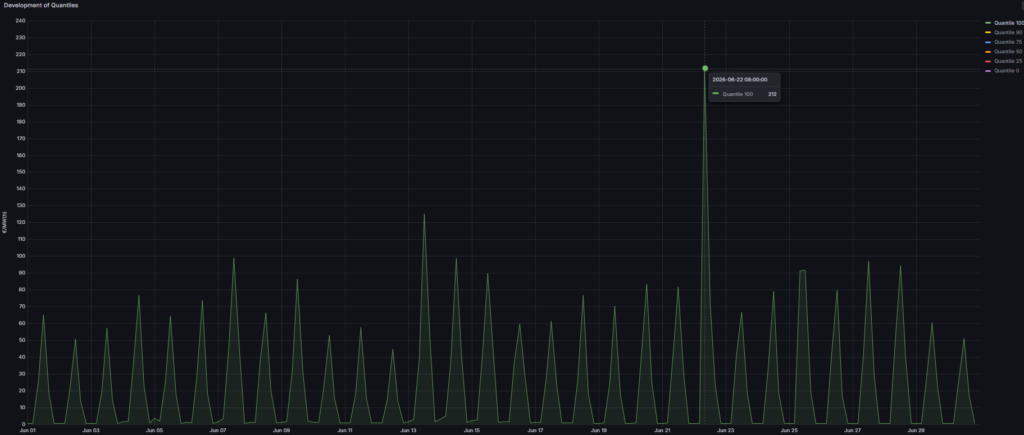

In the aFRR-, the normalization observed after the partly volatile previous months continued consistently. The highest spike of the month occurred on June 22 at 08:00 AM, reaching 212 €/MW/h. Which means that the price remained below the May value of 277 €/MW/h. This calming trend becomes particularly evident in a direct year-over-year comparison: in June 2025, the market was characterized by a massive price surge to over 1000 €/MW/h. In the current reporting month, however, prices apart from the peak on June 22 moved within a stable range of under 125 €/MW/h. This relatively constant fluctuation range provided a reliable environment for algorithmic trading and optimally supported optimization strategies. Our predictive models capitalized on this stable environment with immense precision, driving forecasting performance up to a strong 85%.

The reasons for this pronounced asymmetry between the markets lie, among other things, in the seasonal weather dynamics and the ongoing structural maturation of the energy system. While the expansion of large-scale battery storage stabilized the negative markets even during strong solar feed-in at midday and prevented extreme fluctuations like the previous year, the positive market showed its typical summer vulnerability toward the end of the month. The simultaneous peaks on June 24 at 20:00 illustrate the classic risk of the evening hours, when photovoltaic output drops rapidly while the residual load remains high.

1DA vs. 2DA

Last month’s evaluations confirmed the strategic advantage of the 1-Day-Ahead (1DA) forecast. In a market environment characterized by rising revenues in the positive segments and a consolidation in the negative segment, the shorter forecasting horizon provided the decisive precision. FlexPowerHub translated this agility into higher award rates and significant additional revenues in both countries in direct comparison to the 2-Day-Ahead (2DA) forecast.

The Austrian market showed a highly asymmetric dynamic in June. In the aFRR+, the 1DA forecast achieved a bid acceptance award rate of 91% (2DA: 83%). This led to revenues of 7,046 €/MW/m and an additional revenue of 913 €/MW/m, which exceeds the previous month’s value (643 €/MW/m). In June 2025, the additional revenue was even higher at 1,378 €/MW/m.

In contrast, the 1DA forecast recorded a more moderate additional revenue of just under 274 €/MW/m in the declining aFRR-, with total revenues reaching 10,096 €/MW/m and a bid acceptance rate of 94%. The decline compared to May (1,320 €/MW/m additional revenue) and the previous year (1,651 €/MW/m) reflects the general market stabilization and the decreasing price level.

The German market showed an analogous development. In the aFRR+, the 1DA forecast secured a bid acceptance rate of 93% (2DA: 81%). Financially, this resulted in revenues of 7.818 €/MW/m for the 1DA compared to 6.895 €/MW/m for the 2DA. The additional revenue of 922 €/MW/m significantly exceeded the previous month’s value (582 €/MW/m). In June 2025, extreme price peaks had led to a historic additional revenue of over 11.312 €/MW/m; nevertheless, the current month underlines the advantage of the shorter forecast horizon during upward phases.

In the aFRR-, the additional revenue levelled off at a good 221 €/MW/m due to the market cooling. The 1DA forecast generated revenues of 10.281 €/MW/m with a bid acceptance rate of 92%. Here, too, the comparison with the previous month (629 €/MW/m additional revenue) and June 2025 (1.688 €/MW/m) shows the direct impact of lower market prices on nominal additional revenues. Nonetheless, the 1DA forecast remains the most efficient instrument for optimizing the utilization of available potential across all markets.