Following the pronounced decline already seen in October, the downward trend on the German and Austrian balancing capacity markets continued clearly in November. Revenues were noticeably lower across all markets, while overall volatility eased somewhat but remained clearly visible.

In this edition of our market analysis, we examine the development of marginal prices and revenues in FCR, aFRR and mFRR and compare the Austrian and German markets. We also take a closer look at the performance of FlexPowerHub, focusing on forecast performance, bid acceptance rates and revenue development relative to the market average, and compare our 1-day-ahead forecast with the 2-day-ahead forecast.

We hope you enjoy reading this edition and that the insights provided offer valuable support for your day-to-day operations.

Revenues and marginal prices in November — an overview covering all markets

Throughout November, marginal prices in the balancing capacity markets in Germany and Austria continued to decline noticeably. After the decline already observed in October, price levels fell further in all markets.

In Austria, this downward movement was clearly visible across all markets. In aFRR−, marginal prices fell from 14,177 €/MW/h in October to 5,300 €/MW/h in November. The aFRR+, which had held a comparatively high level of 24,767 €/MW/h in October, declined markedly to 13,035 €/MW/h. Marginal prices in mFRR− also decreased, from 10,577 €/MW/h to 4,534 €/MW/h, while mFRR+ at 4,138 €/MW/h was only slightly below the previous month’s level of 4,711 €/MW/h. In FCR, the downward movement that had already begun in October continued clearly, with revenues falling to a noticeably lower level of 6,786 €/MW/h.

In Germany, marginal prices also moved consistently down in November. In aFRR− they declined from 18,672 €/MW/h in October to 7,803 €/MW/h, and in aFRR+ from 33,423 €/MW/h to 16,674 €/MW/h in November. The mFRR− likewise recorded a clear decrease from 7,339 €/MW/h to 2,122 €/MW/h. The mFRR+ proved somewhat more stable and fell more moderately from 6,527 €/MW/h to 5,198 €/MW/h. In FCR, the development seen in Austria was mirrored. Revenues decreased from 11,586 €/MW/h in October to 6,786 €/MW/h in November, confirming the significantly lower overall level on the balancing capacity markets in both countries.

Comparison of revenues generated with FPH and the market average in the aFRR

In November, the continuous decline in price levels on the balancing capacity markets was clearly reflected in the revenue development in Austria and Germany as well. After the already noticeable decrease in October, aFRR revenues declined again significantly in both countries.

In Austria, revenues in both aFRR- and aFRR+ fell sharply, but remained largely in line with the overall market development, as the market average also decreased clearly. A similar picture emerged in Germany, with declining revenues in both aFRR markets. Despite the overall lower revenue environment, FlexPowerHub was able to maintain its strong operational position and further improve forecasting performance across all markets.

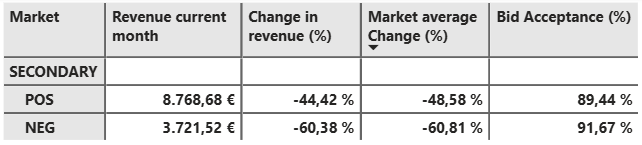

In the Austrian aFRR+ , the revenue level declined noticeably in November. Revenues achieved with FlexPowerHub amounted to 8,769 €/MW/h, compared with 15,777 €/MW/h in October, while the market average also moved lower from 17,922 €/MW/h to 9,215 €/MW/h. Despite this pronounced downward shift, the bid acceptance rate remained high at 89.44 %, even though it decreased by 7.06 %. At the same time, forecasting performance developed very positively and improved from 88 % to 95 % in November.

In the German aFRR+, the picture was somewhat more differentiated. Revenues achieved with FlexPowerHub decreased from 16,075 €/MW/h in October to 10,776 €/MW/h in November. The market average also fell, from 23,149 €/MW/h to 12,081 €/MW/h, and therefore remained above the level achieved with FlexPowerHub. The bid acceptance rate improved by 6.62 % to a very solid 90 %, and forecasting performance rose sharply from 69 % to 89 %, underlining the robustness of FlexPowerHub’s performance in a still demanding market environment.

In the German aFRR-, the downward trend observed in October continued in November. Revenues achieved with FlexPowerHub fell from 10,328 €/MW/h to 4,277 €/MW/h, while the market average decreased from 12,247 €/MW/h to 4,922 €/MW/h and thus confirmed the overall downward market trend. The bid acceptance rate remained at a solid level, although it declined by 9.23 % to 88.33 %. Forecasting performance increased from 84 % to 87 %, indicating a clear positive development despite the lower revenue level.

Market volatility

Volatility in the Austrian and German balancing capacity markets remained clearly visible in November, although overall conditions were somewhat calmer than in October. In Austria, aFRR- was characterised by a markedly lower price level and a clear downward trend over the month, while in aFRR+ pronounced price spikes appeared, particularly toward the end of the period. In Germany, price levels remained broadly moderate for most of November but were interrupted by several distinct swings. Compared with October, extreme peaks were generally less pronounced and the price level in aFRR- in particular shifted noticeably downward, even though short-lived price jumps continued to create a demanding market environment.

Austria:

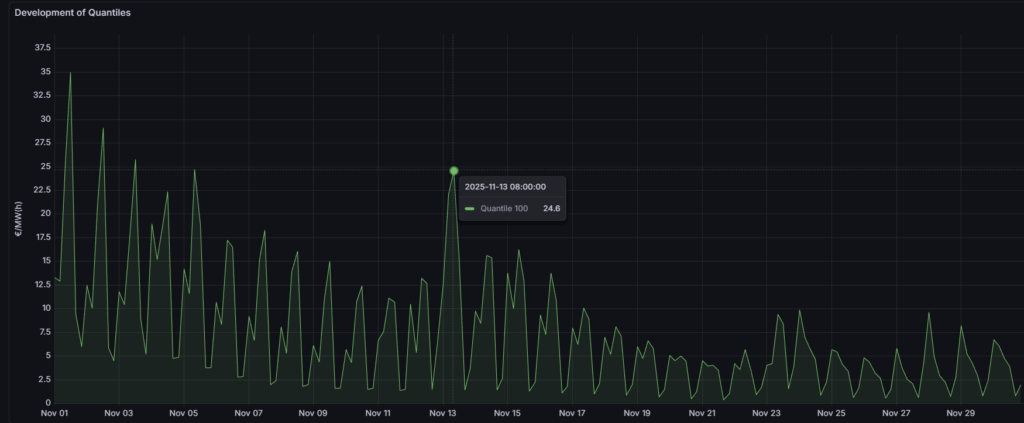

In the Austrian aFRR-, November was noticeably calmer overall than the previous month. The month began with a comparatively high price level of 35 €/MW/h on 1 November. From there, prices followed an almost continuous downward path. This trend was interrupted only briefly on 13 November at 08:00, when prices climbed to 24.6 €/MW/h before resuming their decline. The market reached its lowest level at 0.36 €/MW/h on 21 November and ended the month at 1.95 €/MW/h on 30 November. Compared with October, when several more pronounced movements up to around 75 €/MW/h were observed, November therefore appeared clearly calmer overall, with a lower price level throughout. In this environment, forecasting performance improved slightly to 96 %. This improvement shows that the model captured the smoother downward price trend reliably, despite the brief interruption mid-month.

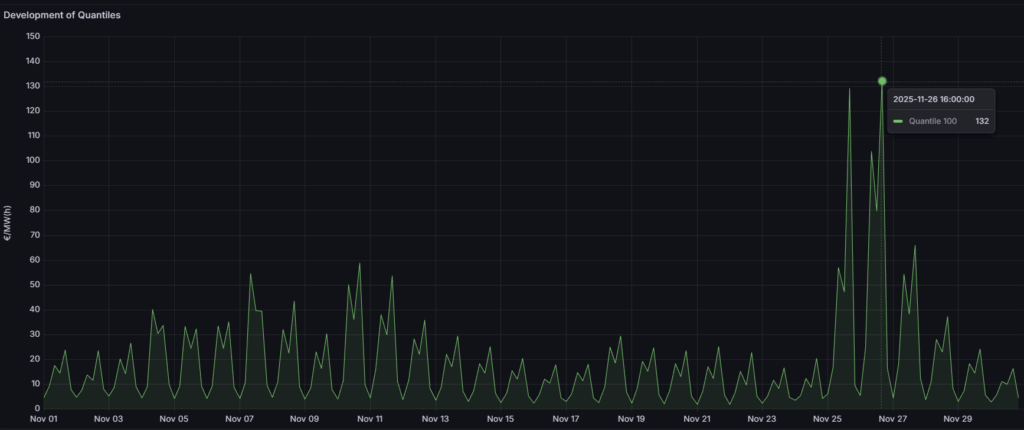

In the Austrian aFRR+ balancing capacity market, November started from a low price level of 4.86 €/MW/h. For most of the month, prices moved within a moderate corridor of roughly 4.1 to 59 €/MW/h, which gave the market a comparatively orderly profile. Only towards the end of the month did dynamics intensify, with two pronounced spikes: 129 €/MW/h on 25 November and the monthly high of 132 €/MW/h on 26 November. After these peaks, prices quickly returned to the levels that had prevailed over large parts of the month. Compared with October, when the monthly high of 180 €/MW/h was already reached at the beginning of the period and several distinct swings followed, the stronger volatility in November was concentrated mainly in the final days. While the most extreme values remained somewhat below the peaks of the previous month, the overall picture was one of a slightly calmer, yet still clearly active market environment. In this market setting, forecasting performance improved noticeably, rising from 88 % in October to 95 % in November. This improvement indicates that the model captured both the largely orderly price pattern and the short-lived spikes at the end of the month more accurately.

Germany:

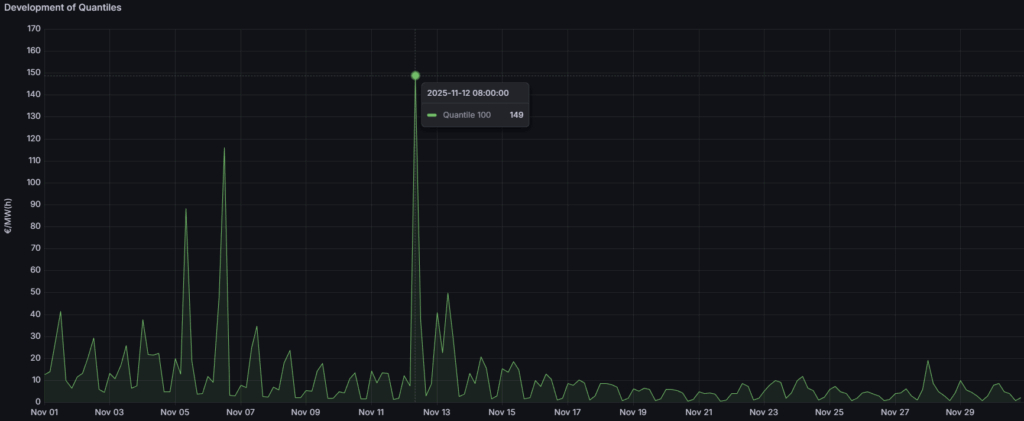

In the German aFRR- balancing capacity market, prices were at a low level for much of November. In many MTUs they remained below 30 €/MW/h, pointing to an overall moderate market environment. However, several pronounced outliers did occur. At the beginning of the month, a price of 88.5 €/MW/h was observed on 5 November, followed by 116 €/MW/h on 6 November. The most notable price spike took place on 12 November, when the price rose from 7.66 €/MW/h at 04:00 to 149 €/MW/h at 08:00, before falling back to 3 €/MW/h by 16:00. Compared with October, when peaks still reached up to 181 €/MW/h and the general level often lay below 90 €/MW/h, prices shifted further downward in November. The number of sharp spikes remained limited, so the market appeared somewhat calmer overall, while still clearly volatile. In this environment, forecasting performance improved slightly from 84 % to 87 %. Our forecasting model thus captured the generally calmer market development, which was still punctuated by individual outliers, with increasing precision.

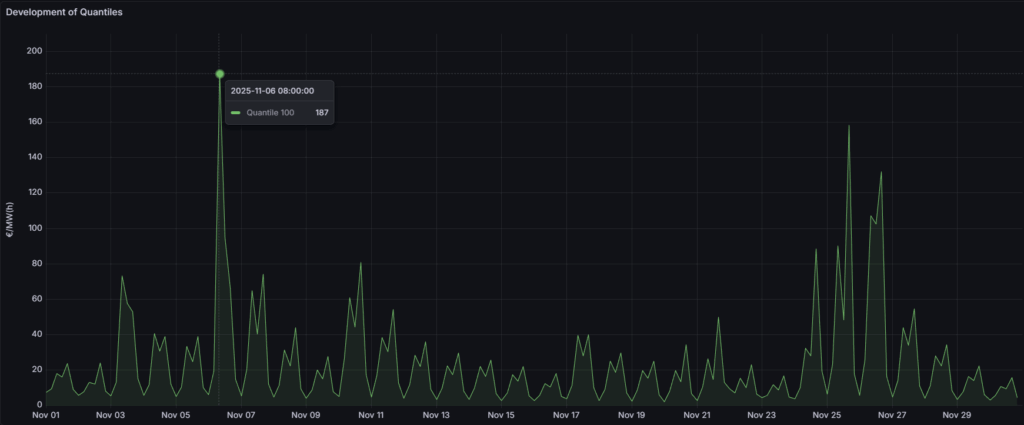

In the German aFRR+ balancing capacity market, prices stayed below 80 €/MW/h for large parts of November. Despite this moderate overall level, several pronounced price spikes occurred. The most notable was on 6 November, when the price rose from 19.2 €/MW/h to 187 €/MW/h within four hours. Further sharp movements were recorded towards the end of the month, with 159 €/MW/h on 25 November followed by 132 €/MW/h on 26 November. Compared with October, when individual extreme peaks reached up to 567 €/MW/h and several large swings shaped the month, the maximum values in November were noticeably more moderate. The market environment was still characterised by occasional and sometimes abrupt price jumps, which continue to require heightened attention in trading and forecasting. In this environment, our forecast performance improved markedly from 69 % in October to 89 % in November. The forecasting model thus captured both the more moderate extremes and the still occasional price spikes with significantly higher precision.

Overall, volatility in November eased somewhat in both countries, but remained a key factor for participation and trading strategies in the balancing capacity markets. Although the general price level was lower, occasional and sometimes abrupt price spikes continued to require accurate forecasting. The improvement in forecasting performance across all segments analysed shows that our forecasting model was able to reliably capture the interplay between a calmer underlying pattern and individual extreme movements.

1DA vs. 2DA

In November, the advantages of the 1-day-ahead (1DA) forecast over the 2-day-ahead (2DA) approach in the aFRR markets became clear once again. Across both countries, 1DA delivered higher bid acceptance rates and noticeably higher revenues, underlining how valuable a shorter forecast horizon is for short-term optimisation.

In Austria, this benefit was particularly visible in aFRR−. The 1DA forecast achieved a bid acceptance rate of 88.33 %, clearly ahead of the 71.11 % reached with 2DA. Based on this, 1DA generated revenues of 3,668 €/MW/h and secured additional revenues of 648 €/MW/h, which corresponds to a revenue advantage of 21 %. In aFRR+, 1DA performed even more strongly in terms of bid acceptance, reaching 97 % compared with 81 % for 2DA. With 8,651 €/MW/h in revenues, this translated into additional revenues of 1,343 €/MW/h, or an 18 % increase relative to 2DA.

In Germany, the picture was even more favourable for 1DA. In aFRR−, the 1DA bid acceptance rate reached 94 %, while 2DA remained at 77 %. Revenues with 1DA amounted to 4,318 €/MW/h and were 1,031 €/MW/h higher than with 2DA, equivalent to a revenue advantage of 31 %. In aFRR+, 1DA achieved a bid acceptance rate of 92 % compared with 83 % for 2DA. Here, 1DA revenues came to 10,548 €/MW/h and were 2,575 €/MW/h higher than with 2DA, corresponding to a 32 % increase.

From a revenue perspective, the most attractive segment in November was the German aFRR+, where the 1DA setup achieved the highest absolute revenues at 10,548 €/MW/h, together with a substantial revenue advantage of 2,575 €/MW/h over 2DA. For asset owners aiming to maximise earnings, this combination of strong bid acceptance and high absolute revenue levels is particularly relevant. Overall, the November results once again confirm that a 1-day-ahead forecasting approach strengthens market responsiveness and helps capture more of the available revenue potential across all aFRR markets, especially in volatile conditions.