Revenues and marginal prices in October — an overview covering all markets

Balancing capacity prices in Austria and Germany eased noticeably in October after the strong increases observed in September. Most market recorded lower marginal prices, indicating a partial correction of the sharp late-summer surge. While the aFRR+ in Austria remained stable at a high level, other segments showed clear signs of normalization. A similar picture emerged in Germany, where both positive and negative markets returned to more moderate price ranges.

In October, the development on the balancing capacity markets showed a noticeable easing compared to the previous month. After the sharp price increases seen in September, most market segments in Austria and Germany recorded declining marginal prices. This suggests a partial correction of the strong upward trend that had dominated late summer.

In Austria, the downward movement was most apparent in the negative market segments. Marginal prices in the aFRR- fell to 14,177 €/MW/h, after reaching 18,253 €/MW/h in September. The aFRR+ remained largely stable and only showed a slight increase to 24,767 €/MW/h, confirming its position at a high level. The mFRR- recorded a stronger correction to 10,577 €/MW/h, while the mFRR+ remained almost unchanged at 4,711 €/MW/h. In the FCR market, revenues generated with FlexPowerHub continued to ease, declining to 11,708 €/MW/h after 12,470 €/MW/h in the previous month.

In Germany, the market followed a similar trend. Marginal prices in the aFRR- decreased to 18,672 €/MW/h, while the aFRR+ fell to 33,423 €/MW/h, both segments showing a return to more moderate levels after September’s peak values. The mFRR- dropped noticeably to 7,339 €/MW/h, and the mFRR+ also moved lower to 6,527 €/MW/h. In the FCR, a slight decline of revenues to 11,586 €/MW/h was observed, continuing the calm development already seen in Austria.

Overall, October was characterized by a normalization of price levels across both markets. After the pronounced increases in September, maginale prices in the balancing capacity markets have settled at a more stable level, particularly in Germany.

Comparison of revenues generated with FPH and the market average in the aFRR

In the Austrian aFRR+, October brought a continuation of the positive revenue trend. FlexPowerHub achieved 15,777 €/MW/h, slightly above the previous month’s level of 15,069 €/MW/h. The overall market also expanded, with the average rising to 17,922 €/MW/h. The bid acceptance rate improved by 7.59% to 96.2% for the forecasted 50% Quantile, showing strong market participation. Forecast performance remained steady at 88%, once again demonstrating reliable forecast quality under continuously dynamic market conditions.

Revenues achieved with FlexPowerHub in the aFRR- in Austria decreased noticeably in October and reached 9,393 €/MW/h. This represents a decline of around 30% compared to the previous month. The market average followed a similar pattern and dropped to 9,876 €/MW/h. Despite the weaker revenue development, operational performance remained strong. The bid acceptance rate increased by 8.34% to a high level of 95.7%. Forecast performance stayed strong at 95%, reflecting a stable model performance even in a lower-priced market environment.

In Germany, revenues achieved with FlexPowerHub in aFRR- declined to 10,328 €/MW/h after reaching 17,242 €/MW/h in September. This development reflects the overall cooling of the German market, where the average also dropped from 19,655 €/MW/h to 12,247 €/MW/h. Despite lower revenues, FlexPowerHub maintained strong operational results. The bid acceptance rate rose slightly to 97.31%, confirming stable market access and consistent participation. Forecast performance reached 84.33%, remaining at a good level.

In the German aFRR+, October results showed a slight correction after the strong increase observed in September. Revenues achieved with FlexPowerHub reached 16,075 €/MW/h, slightly below the previous month’s 16,813 €/MW/h. The market average followed the same trend and decreased from 24,491 €/MW/h to 23,149 €/MW/h. The bid acceptance rate fell by 2.61% to 84.41%, while forecast performance decreased to 69.42%. Despite the challenging environment, FlexPowerHub continued to perform reliably and was able to maintain a stable revenue position within a still volatile market context.

Market volatility

October continued to show a high level of volatility across the Austrian and German balancing markets, although with a calmer overall trend compared to September. In Austria, price movements were moderate and more evenly distributed, reflecting a steady but still active market environment. In Germany, however, several distinct price peaks, particularly in aFRR+, again created temporary pressure on forecast performance and market stability. Despite these fluctuations, overall forecast accuracy remained robust, demonstrating the model’s ability to adapt effectively even under persistent volatility. These results underline the ongoing importance of precise forecasting to maintain reliable operations in an increasingly dynamic market landscape.

Austria:

In the aFRR-, October remained characterized by volatility, although no extreme price spikes occurred. Prices ranged between €1.42/MW/h and €75/MW/h. The month started with a moderate peak of around €75/MW/h on October 4 at 12:00, followed by a gradual decline. On October 11, prices briefly increased from €5.81/MW/h to €61.5/MW/h within a few hours. Afterwards, the market remained largely stable despite minor fluctuations, before reaching another slightly stronger peak of €65.1/MW/h on October 24.

Compared to September, volatility remained noticeable, although the overall price level was lower. Our forecast captured the market movements very well and once again achieved a strong performance of 96%.

In the aFRR+, October proved to be more active overall than September. Prices ranged between €4.89/MW/h and €180/MW/h, with the month’s peak of €180/MW/h recorded on October 1 at 16:00. During the month, several distinct fluctuations occurred, such as on October 21, when the price rose from €5.44/MW/h at 00:00 to €127/MW/h at 08:00 before gradually declining again. Aside from the peak on October 1, the general price level remained largely unchanged compared to September. However, these isolated movements resulted in a slightly higher overall volatility throughout the month.

Our forecast remained stable and was able to capture the volatile market conditions reliably. With a performance of 88.1%, it stayed almost at the same level as in September.

Germany:

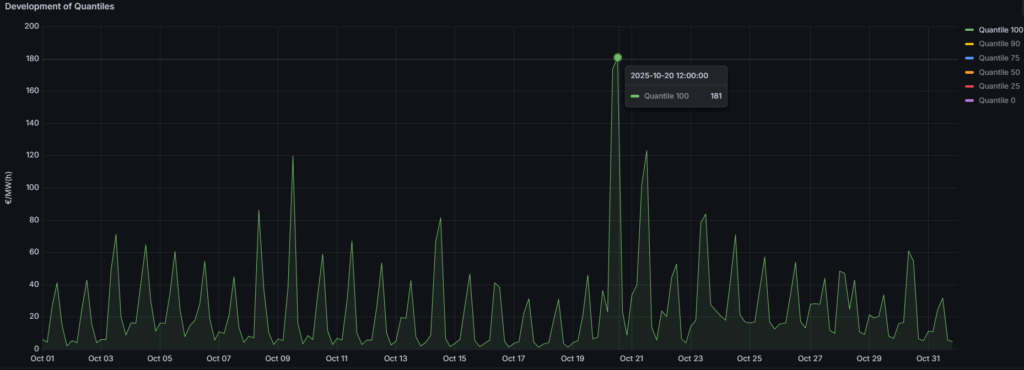

In the aFRR- segment, October was noticeably calmer overall and did not reach the high price levels of the previous month. Nevertheless, a few price spikes were observed. The most significant movement occurred on October 20, when the price rose from €23.2/MW/h at 04:00 to €181/MW/h at 12:00. Apart from two smaller peaks on October 9 (€120/MW/h) and October 21 (€123/MW/h), prices remained largely stable at levels below €90/MW/h.

Compared to September, market volatility remained noticeable but appeared less abrupt and did not reach the extreme levels of the previous month. Our forecast captured the market movements reliably and achieved a solid performance of 84.6%, although slightly below the previous month’s result.

In the aFRR+ segment, October once again showed a restless market environment, though without the extreme price spikes seen in September. Several pronounced fluctuations shaped the month’s development. The most notable occurred on October 8, when the price rose from €10/MW/h at 00:00 to €567/MW/h at 08:00. Another peak was recorded on October 13 at €287/MW/h, followed by a further increase on October 20 at 08:00, reaching €219/MW/h. Apart from these movements, the overall price level remained consistently below €197/MW/h.

Compared to the previous month, volatility remained elevated but appeared more balanced overall. Our forecast responded steadily to the changing market conditions and achieved a slight improvement, reaching 72.4% compared to the highly challenging September.

1 dayahead vs. 2 daysahead Forecasts

October once again demonstrated the clear benefits of using a 1-Day-Ahead forecast (1DA) compared to a 2-Day-Ahead forecast (2DA) in the aFRR markets. Across both Austria and Germany, the 1DA approach continued to deliver higher bid acceptance rates and stronger revenue outcomes, confirming its importance for short-term optimization.

In Austria, the advantage of the 1DA forecast was particularly evident. In aFRR-, the 1DA achieved a bid acceptance rate of 94.62%, far exceeding the 78.49% of the 2DA. This difference translated into additional revenues of 1,641 €/MW/h, corresponding to a 22% increase. The effect was even stronger in aFRR+, where the 1DA reached a bid acceptance rate of 94% compared to 77% for the 2DA, resulting in an additional 3,432 €/MW/h or 28% higher revenues.

Germany followed a similar trend, with both aFRR segments showing clear improvements when using the 1DA forecast. In aFRR-, the 1DA achieved 94% versus 90% for the 2DA, leading to an additional 937 €/MW/h, equivalent to a 10% increase. The most pronounced effect was observed in the aFRR+, where the 1DA reached a bid acceptance rate of 92% compared to only 80% for the 2DA. This resulted in additional revenues of 3,921 €/MW/h, representing a 31% increase and marking the highest relative benefit across all comparisons.

Overall, the October results once again confirm that shorter forecast horizons significantly enhance market responsiveness and revenue potential. The 1-Day-Ahead forecast proved most advantageous in Germany’s aFRR+, where its higher precision translated directly into substantial financial gains.