Revenues and marginal prices — an overview covering all markets

Overall, January extended the calmer tone already seen in December across the German and Austrian balancing capacity markets. Marginal prices in the aFRR softened further in both countries, while the mFRR delivered a more mixed picture. At the same time, the FCR rebounded noticeably, reversing the downward trend of the previous month. Despite the weaker aFRR price environment and lower revenues compared to December, our performance remained broadly stable with consistently high bid acceptance rates.

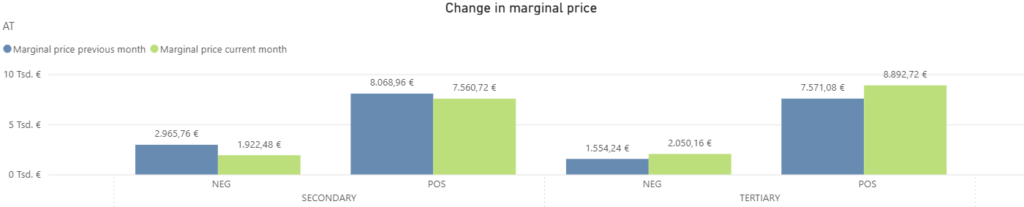

In Austria, the decline remained clearly visible in both directions. In the aFRR-, marginal prices fell from 2,966 €/MW/h in December to 1,922 €/MW/h in January. The aFRR+ prices also moved lower, easing from 8,069 €/MW/h to 7,561 €/MW/h. By contrast, the mFRR prices shifted upward. On the negative side, marginal prices increased from 1,554 €/MW/h to 2,050 €/MW/h, and on the positive side they rose from 7,571 €/MW/h in December to 8,893 €/MW/h in January. The most pronounced change was seen in FCR, where revenues climbed sharply to 8,863 €/MW/h, up 77% from 4,997 €/MW/h in December.

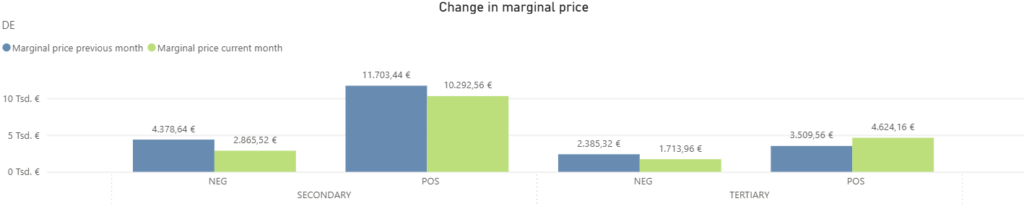

In Germany, the same downward trend prevailed in the aFRR. Marginal prices moved lower in both directions, with aFRR- falling from 4,379 €/MW/h in December to 2,866 €/MW/h in January and aFRR+ easing from 11,703 €/MW/h to 10,293 €/MW/h. In the mFRR, the picture was more differentiated. On the negative side, marginal prices decreased from 2,385 €/MW/h to 1,714 €/MW/h, while the positive side recovered after a weaker December and rose from 3,510 €/MW/h to 4,624 €/MW/h. FCR also showed a clear improvement in January, with revenues increasing by 49% to 7,293 €/MW/h.

Comparison of revenues generated with FPH and the market average in the aFRR

In January, the noticeably calmer aFRR market environment already seen in December continued. In both countries, revenues generated with FlexPowerHub and the market averages declined, reflecting the still subdued market dynamics. At the same time, bid acceptance rates and forecast performance stayed at a good level.

Austria

In Austrian aFRR+, revenues generated with FlexPowerHub fell noticeably to 4,446 €/MW/h in January, after reaching 5,740 €/MW/h in December. Since the market average also declined over the same period from 6,010 €/MW/h to 5,440 €/MW/h, our performance remained aligned with the overall market trend. This development was accompanied by a largely stable bid acceptance rate, coming in at 87% in January compared to 89% in the previous month. Forecast performance declined to 82%, highlighting the more challenging optimization environment currently seen in the positive segment.

In parallel, the downward movement continued in Austrian aFRR-, with revenues falling from 1,709 €/MW/h in December to 1,229 €/MW/h in January. Here as well, results followed the market average, which decreased from 1,677 €/MW/h to 1,247 €/MW/h. Despite the overall lower price level, market access remained very solid, supported by an 88% bid acceptance rate. Particularly noteworthy is the forecast performance, which at 99% after 102% in December continues to confirm excellent accuracy and shows that our model can capture market movements precisely.

In the German aFRR+ market, revenues generated with FlexPowerHub corrected to 5,194 €/MW/h in January, after reaching 6,419 €/MW/h in December. This development ran in parallel with the market average, which fell from 7,848 €/MW/h to 7,064 €/MW/h. Despite the overall weaker price environment, market access in the positive segment strengthened significantly, reflected in a bid acceptance rate rising to 96% compared to 85% in December. Forecast performance declined to 74% in this challenging environment, down from 82% in the previous month.

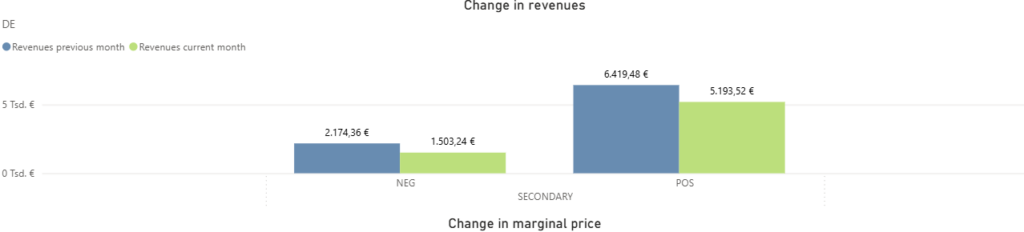

The aFRR- also showed a clear decline. Revenues achieved with FlexPowerHub dropped from 2,174 €/MW/h in December to 1,503 €/MW/h in January. The market average fell in parallel from 2,535 €/MW/h to 1,963 €/MW/h, meaning revenue development again followed the market trend. The bid acceptance rate decreased in January to 87%, down from 91% in December. Forecast performance also weakened, coming in at 77% compared to 86% in the previous month.

Market volatility

In January, aFRR in Austria and Germany continued to operate in a predominantly calm market environment with low price levels. Volatility remained mostly contained across all segments, but was punctuated by a few clearly defined price spikes and, in the aFRR+ markets, by recurring strong swings. Notably, both countries recorded a pronounced spike in aFRR- on 9 January. While Austria reached its monthly high on that day, Germany also saw the strongest swing of the month. Compared to December, the underlying price level in aFRR- remained low in both countries, while aFRR+ was overall more unsettled in January, with swings occurring more frequently and spread more evenly across the month.

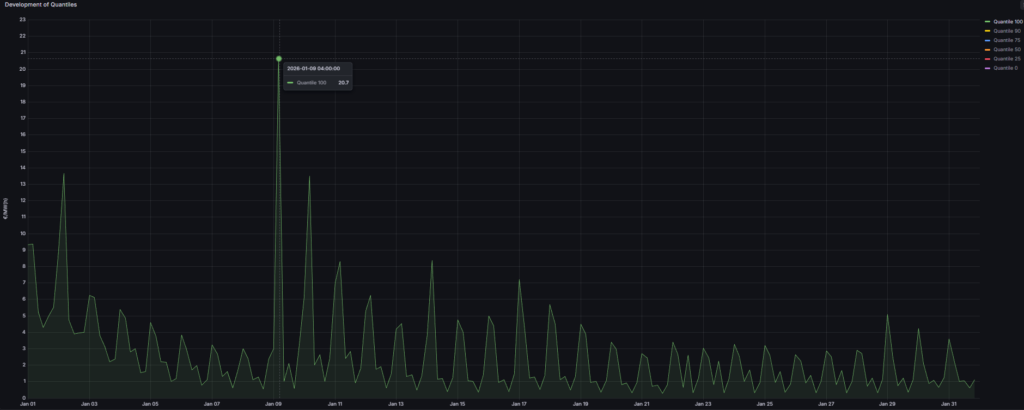

In Austrian aFRR-, January was characterized by a very low and stable price level for most of the month. In the majority of time blocks, prices remained below 10 €/MW/h, reflecting a generally calm market environment. This stable baseline was interrupted on only a few days by clearly visible price spikes that temporarily increased volatility.

An initial spike occurred at the beginning of the month on 2 January, when prices briefly rose from below 6 €/MW/h to 13.7 €/MW/h. The most pronounced movement followed on 9 January, when the monthly high of 20.7 €/MW/h was reached. On 10 January, another peak of 13.5 €/MW/h was observed, before prices fell back below 10 €/MW/h and the market returned to a calm pattern.

Compared to December, which saw higher extremes up to 49 €/MW/h, January was clearly more moderate and was more strongly defined by a consistently low baseline. In this environment, market access remained stable. The bid acceptance rate came in at 88% and forecast performance at 99%, indicating that FlexPowerHub was able to capture the combination of a calm baseline and a few short-lived outliers reliably.

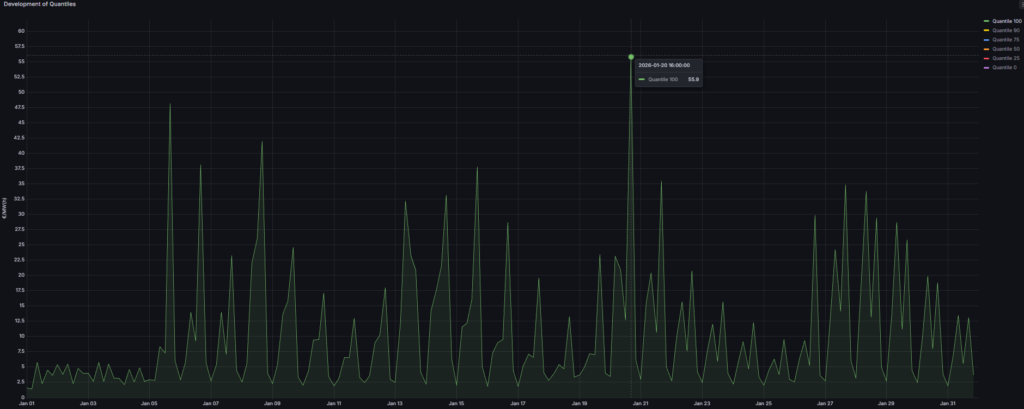

In Austrian aFRR+, January started with a very low price level, below 6 €/MW/h. Thereafter, prices increased and the remainder of the month was characterized by recurring strong fluctuations. The market pattern was therefore less driven by isolated outliers and more by a repeated cycle of very low price levels followed by abrupt spikes.

The first notable spike occurred on 5 January, when prices briefly jumped from 7 €/MW/h to 48 €/MW/h and then quickly returned to around 6 €/MW/h. This pattern continued throughout large parts of the month. The maximum value was recorded on 20 January, when prices rose briefly from 13 €/MW/h to 56 €/MW/h.

Compared to December, when volatility was more concentrated at the start of the month and the market became calmer afterwards, January remained more variable throughout. At the same time, the monthly high stayed below the December extreme of 74 €/MW/h. The bid acceptance rate was 87% and forecast performance 82%, reflecting the higher operational demands created by frequent and abrupt swings.

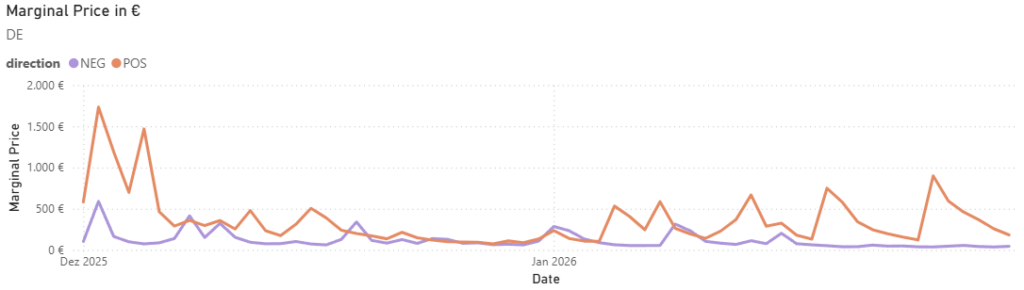

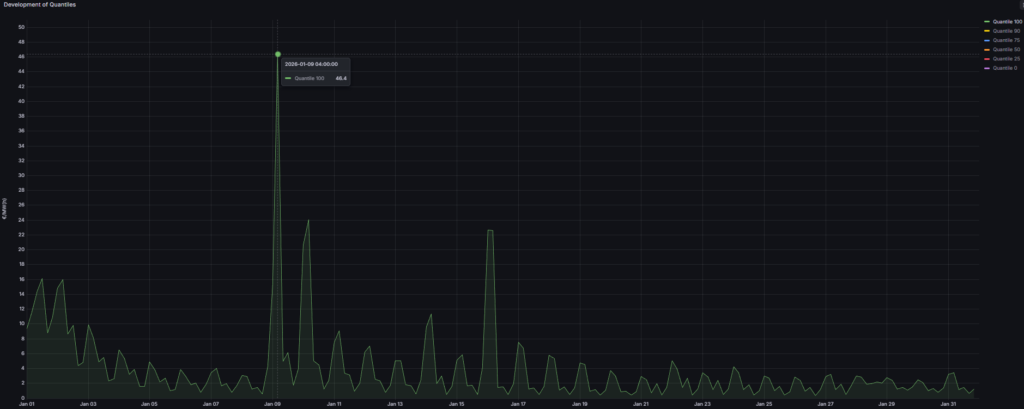

In the German aFRR-, January showed a very low price level below 9 €/MW/h for the majority of the month. Overall volatility remained limited, but was clearly interrupted by some pronounced price spikes.

The first and highest spike occurred on 9 January, when prices rose briefly from around 15 €/MW/h to 46 €/MW/h and then quickly fell back to around 5 €/MW/h. Already the following day, prices increased again to 24 €/MW/h. Another clear spike was observed on 16 January at 23 €/MW/h. After that, the market stabilized again and remained on the low baseline through month end.

Compared to December, which featured several spikes up to 69 €/MW/h, January was more moderate and returned to calm conditions more quickly. The bid acceptance rate was 87% and forecast performance 77%, indicating that the model captured the calm baseline well, while the few but pronounced peaks increased the forecasting challenge.

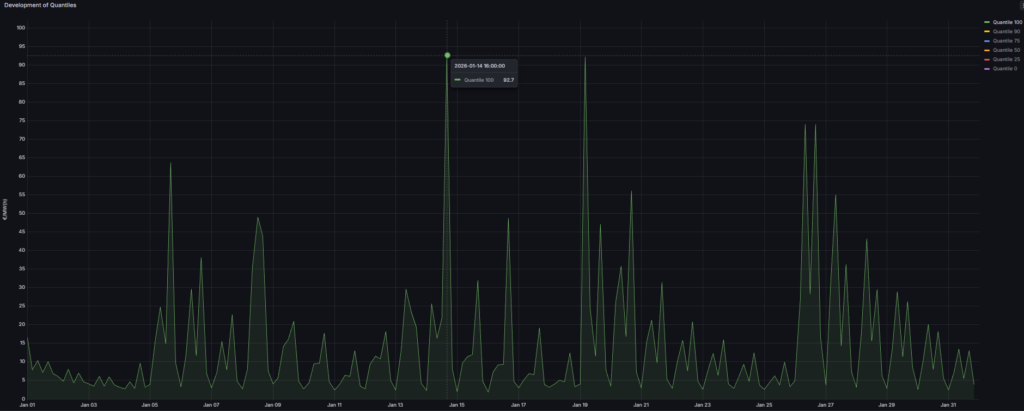

In the German aFRR+, January started at a low level below 20 €/MW/h before numerous clearly pronounced price spikes occurred over the course of the month. While the baseline remained moderate over many products, it was repeatedly interrupted by short-lived jumps, increasing volatility throughout the month.

A first pronounced peak occurred on 5 January at 64 €/MW/h. The highest values were reached on 14 and 19 January, when prices briefly rose to around 92 €/MW/h. Toward the end of the month, another strong fluctuation was observed on 26 January, when prices first increased to 74 €/MW/h, then dropped to 28 €/MW/h, and rose again to 74 €/MW/h. After that, price levels stepped down gradually.

Compared to December, the absolute extremes were much lower, as the exceptional spikes up to around 257 €/MW/h did not occur. At the same time, volatility in January was spread more evenly across the month and was less concentrated at the beginning. The bid acceptance rate reached 96%, remaining at a very high level. Forecast performance came in at 74%, showing that recurring and sometimes abrupt peaks continued to create demanding conditions for short-term forecasting.

1DA vs. 2DA

In January 2026, the aFRR markets showed a clear advantage of the 1-day-ahead forecast compared to the 2-day-ahead forecast. In Austria as well as in Germany, the shorter forecast horizon led to higher bid acceptance rates and, in turn, noticeably higher revenues. Especially in a market environment that was largely characterized by low price levels and only occasional sharp swings, the improved short-term adaptability of the 1DA approach proved valuable once again.

In January 2026, the aFRR markets showed a clear advantage of the 1-day-ahead forecast compared to the 2-day-ahead forecast. In Austria as well as in Germany, the shorter forecast horizon led to higher bid acceptance rates and, in turn, noticeably higher revenues. Especially in a market environment that was largely characterized by low price levels and only occasional sharp swings, the improved short-term adaptability of the 1DA approach proved valuable once again.

In Austria, the added value of 1DA was confirmed in both directions. In aFRR-, 1DA achieved a bid acceptance rate of 89.78% compared to 69.35% for 2DA. Revenues amounted to 1,198.12 €/MW/month, representing an additional 306.36 €/MW/month versus 2DA. In aFRR+, the advantage was similarly clear. 1DA reached a bid acceptance rate of 93.55% compared to 70.97% for 2DA. On this basis, revenues of 4,707.16 €/MW/month were achieved, corresponding to an uplift of 1,227.48 €/MW/month.

In Germany, the 1DA advantage was also clearly visible. In aFRR-, the bid acceptance rate stood at 86.56%, while 2DA reached 68.28%. Revenues totalled 1,517.00 €/MW/month, which is 468.08 €/MW/month higher than 2DA. In aFRR+, the revenue gap was once again particularly pronounced. Here, 1DA achieved a bid acceptance rate of 93.55% compared to 79.03% for 2DA. At the same time, revenues of 5,234.88 €/MW/month were generated, resulting in an uplift of 1,219.88 €/MW/month versus 2DA.

From a revenue perspective, German aFRR+ was again the most attractive market in January. It combined the highest absolute revenues of 5,234.88 €/MW/month with a clear advantage over the 2DA approach. Overall, the January results once more confirm that the 1DA forecast supports short-term optimization and can unlock a larger share of the available revenue potential.