Revenues and marginal prices in December — an overview covering all markets

In December, the downward trend in marginal prices across the German and Austrian balancing capacity markets persisted, confirming the lower price environment observed in recent weeks. Across both countries, the majority of market values settled below their November levels.

In Austria, the decline remained pronounced. In aFRR-, marginal prices fell significantly from 5,300 €/MW/h in November to 2,966 €/MW/h in December. The aFRR+ followed suit, with prices retreating by approximately 5,000 €/MW/h to settle at 8,069 €/MW/h. A sharp contraction was also noted in mFRR-, where values dropped from 4,534 €/MW/h to 1,554 €/MW/h. Conversely, mFRR+ bucked the trend, rising from 4,138 €/MW/h in November to 7,571 €/MW/h. FCR prices also continued to ease, decreasing from 6,786 €/MW/h to 4,997 €/MW/h.

In Germany, marginal prices largely mirrored this downward trajectory. In aFRR-, prices declined from 7,803 €/MW/h in November to 4,379 €/MW/h, while aFRR+ dropped from 16,674 €/MW/h to 11,703 €/MW/h. The mFRR- provided a slight exception, coming in at 2,385 €/MW/h, which was slightly above the November value of 2,122 €/MW/h. Meanwhile, mFRR+ saw a more noticeable decrease from 5,198 €/MW/h to 3,510 €/MW/h. Finally, FCR marginal prices tracked lower, reaching 4,900 €/MW/h compared to 6,786 €/MW/h in the previous month.

Comparison of revenues generated with FPH and the market average in the aFRR

The overall calmer market environment on the balancing capacity markets in Germany and Austria continued to impact the development of aFRR revenues in December. Both the revenues achieved with FlexPowerHub and the broader market average settled below the previous month’s levels. The concurrently declining marginal prices in aFRR further underline the weakened market momentum at year-end.

AT:

In the Austrian aFRR+, revenues achieved with FlexPowerHub contracted noticeably to 5,740 €/MW/h in December, down from 8,769 €/MW/h in November. The market average followed a similar pattern, decreasing to 6,010 €/MW/h. Overall, revenue development with FlexPowerHub therefore remained in line with the broader market trend. Compared to the previous month, the bid acceptance rate remained broadly stable, declining only slightly by 0.82% to 88%. Our forecast performance remained unchanged at a high 95%, underscoring the consistent quality of our predictions

The decline in aFRR- was even more pronounced. December revenues via FlexPowerHub reached 1,709 €/MW/h, compared to 3,722 €/MW/h in November. The market average also retreated sharply from 3,870 €/MW/h to 1,677 €/MW/h, reflecting the persistent price pressure in this market. Despite this, market access remained firm with a bid acceptance rate of 89%. A particularly positive development was forecast performance, which improved from 96% to 102%, highlighting our very strong forecast quality even in a weaker price environment.

In the German aFRR+, revenues generated with FlexPowerHub decreased to 6,419 €/MW/h in December, down from 10,776 €/MW/h in November. The market average similarly dropped to 7,848 €/MW/h, signaling a significantly weaker environment. While the bid acceptance rate eased by 5% to 85%, it remained at a healthy level. At the same time, forecast performance declined from 89% to 82%, reflecting the more challenging conditions in the significantly weaker market environment.

A similar pattern emerged for aFRR- in Germany. FlexPowerHub revenues declined to 2,174 €/MW/h from 4,277 €/MW/h in November, mirroring the market average’s fall to 2,535 €/MW/h. This confirms the widespread downward trend also seen in marginal prices. Bid acceptance developed positively, increasing by 2.86% to 91%, underlining our continued stable market access. Forecast performance, while slightly below the previous month at 86%, remained at an overall solid level.

Market volatility

In December, the aFRR markets in Austria and Germany maintained a calm trajectory for the majority of the month, with predominantly low price levels. Volatility remained largely contained, but was shaped by a few clearly defined price spikes. The start of the month stood out in particular, with isolated strong upward moves in both aFRR+ and aFRR-, before the markets stabilised noticeably over the remainder of the month. Compared to November, aFRR- spikes were generally more moderate, whereas a very high extreme value in the German aFRR+ at the beginning of the month drove a short term increase in volatility.

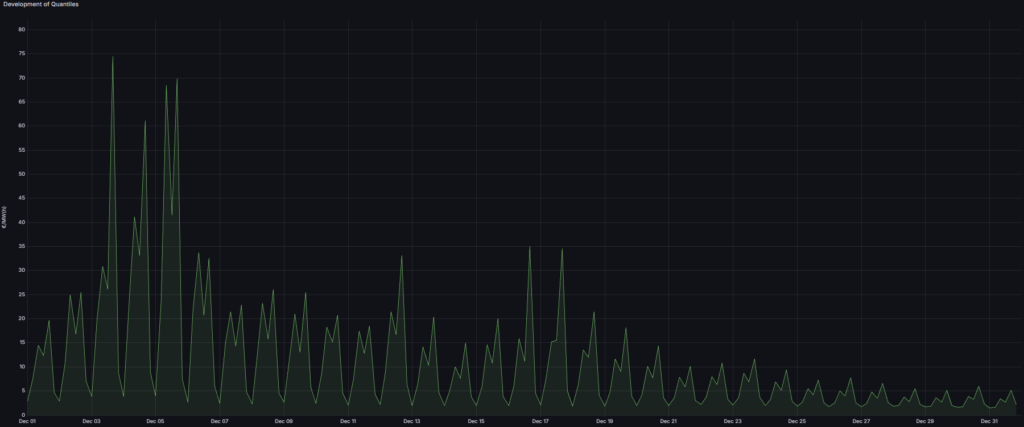

In Austrian aFRR-, prices remained low and stable for most of December, with values frequently settling below 10 €/MW/h, indicating an overall calm market environment. However, this stable baseline was interrupted by occasional short-term spikes, which increased volatility noticeably at specific points.

The first spike occurred on 2 December, when the price rose briefly to 26 €/MW/h. The second and strongest movement followed on 8 December, when the monthly high of 49 €/MW/h was reached. On 19 December, another clear spike occurred, with prices again rising well above the typical level to 32 €/MW/h. After each of these events, the market returned swiftly to its low-price regime and continued with a calm and steady pattern.

In contrast to November, December was dominated by a low and steady baseline, with volatility driven mainly by a few short-lived spikes rather than a sustained price movement. In this setting, reliable market access becomes a key prerequisite for consistent participation. With a solid bid acceptance rate of 89% and an exceptional forecast performance of 102%, our model proved highly reliable in capturing both the calm baseline and these isolated outliers.

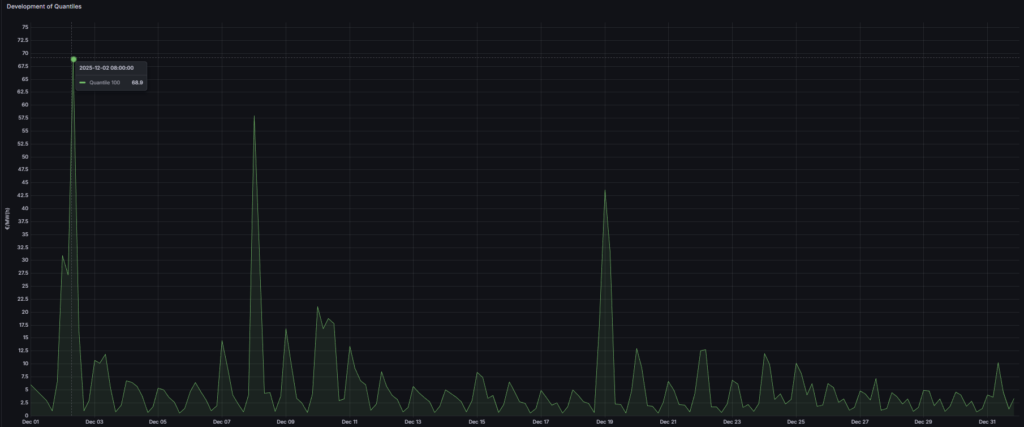

The Austrian aFRR+ market was notably calmer than in November, despite a volatile opening phase. As early as 3 December, a pronounced spike occurred, reaching the monthly high of 74 €/MW/h. In the following days, further clearly visible peaks were observed, with values around 60 to 70 €/MW/h. After this volatile start, prices fell back quickly each time and the market returned to a significantly lower baseline level.

From the second week of the month onwards, moderate price levels dominated, with regular but clearly smaller fluctuations. Isolated increases were still visible, but remained well below the extreme values seen in the first days. In the second half of the month, the market continued to calm further. Prices mostly remained at a low level and pronounced price spikes no longer occurred.

Compared to November, December’s extremes were noticeably lower and largely confined to just a few days at the start of the month.

This structure of a small number of high spikes early in the month followed by an increasingly calm period placed higher demands on our forecasting. Even so, our bid acceptance rate remained solid at 88%. Forecast performance also stayed stable at 95%, confirming that our model delivered robust results during the volatile start and captured the subsequent market stabilisation reliably.

In German aFRR-, December remained at a low and comparatively stable price level for most of the month, but was interrupted by a few clearly defined price spikes. After a calm start with prices in the low single digit range, a strong upward move occurred already on the morning of 2 December, reaching 69 €/MW/h. Prices then fell back quickly and returned to the low range.

Another pronounced spike followed on 8 December, when the price rose briefly again to 58 €/MW/h. After that, the market remained largely calm until mid-month, with smaller and regularly recurring fluctuations. On 19 December, another peak was observed, reaching 44 €/MW/h and thus standing out clearly above the typical baseline. In the second half of the month, the market continued to calm further, spikes became less frequent and generally less pronounced, and the month ended at a low price level.

Compared to November, the baseline remained low in December, but overall the spikes were noticeably more moderate. While several extreme outliers of up to 149 €/MW/h were observed in November, December’s peaks stayed clearly below that level and occurred less frequently. In this environment, FlexPowerHub was able to further strengthen market access. The bid acceptance rate increased by 2.86% and reached 91% in December. At the same time, forecast performance remained largely stable at 86%, only slightly below the November level. This indicates that our model captured the calm baseline reliably while also reflecting the few, but pronounced price spikes robustly in the forecast.

In German aFRR+, December exhibited a distinct two-phase pattern. For large parts of the month, prices stayed at a moderate level and were mostly below 50 €/MW/h. At the same time, this calm baseline was disrupted at the beginning of the month by several signifikant price spikes, which strongly shaped volatility in the first part of December.

Already on 2 December in the early morning hours, an exceptional spike occurred, reaching the monthly high of around 257 €/MW/h. In the following days, volatility remained elevated, with further marked peaks repeatedly reaching a range between 120 and 160 €/MW/h. After this phase, prices declined again, and from the second week of the month onwards a more stable pattern emerged. While isolated increases of 50 to 70 €/MW/h still occurred around mid-month, clearly lower prices dominated overall, often at a level below 30 €/MW/h. In the second half of the month, the market continued to calm further. No notable price spikes were observed anymore, and the market was mainly characterised by small and regular fluctuations.

Compared to November, the baseline remained moderate for many hours in December as well, but the extreme values were significantly higher and concentrated strongly in the first week. These abrupt price jumps placed high demands on our forecasting models and are also reflected in the performance figures. The bid acceptance rate declined by 5% to 85%, but still remained at a solid level. Forecast performance reached 82% in December, below the November value of 89%, largely driven by the exceptionally strong and short term spikes at the beginning of the month.

1DA vs. 2DA

In December, the 1-day-ahead forecast again demonstrated a clear advantage over the 2-day-ahead approach in the aFRR markets. In Austria as well as in Germany, the shorter forecast horizon resulted in higher bid acceptance rates and therefore in noticeably higher revenues. Especially in a market environment that was calm for long periods and only occasionally interrupted by price spikes, the improved short term responsiveness of 1DA paid off once more.

In Austria, the added value of 1DA was confirmed in both directions. In aFRR-, 1DA achieved a bid acceptance rate of 90.86% compared to 75.27% for 2DA. Revenues reached 1,646.20 €/MW/h, corresponding to an additional 288.40 €/MW/h and a revenue advantage of 21.24% versus 2DA. In aFRR+, the advantage was also clear. 1DA reached a bid acceptance rate of 92.47% compared to 70.97% for 2DA. On this basis, revenues of 5,657.80 €/MW/h were achieved, resulting in an additional 828.92 €/MW/h compared to the 2DA approach.

In Germany, the advantage of 1DA was even more pronounced. In aFRR-, the bid acceptance rate was 90.32%, while 2DA reached only 77.42%. Revenues totalled 2,190.36 €/MW/h, which is 507.16 €/MW/h above 2DA and corresponds to a revenue advantage of 30.13%. In aFRR+, a clear advantage was also evident. Here, a bid acceptance rate of 79.57% was achieved compared to 64.52% for 2DA. At the same time, revenues of 6,033.36 €/MW/h were realised, resulting in an additional 1,315.36 €/MW/h versus 2DA and a revenue advantage of 27.88%.

From a revenue perspective, German aFRR+ was therefore the most attractive market in December. Here, 1DA generated the highest absolute revenues of 6,033.36 €/MW/h with a clear lead over 2DA. Overall, the December results once again confirm that the 1DA forecast supports short term optimisation and helps capture a larger share of the available revenue potential.