Revenues and marginal prices — an overview covering all markets

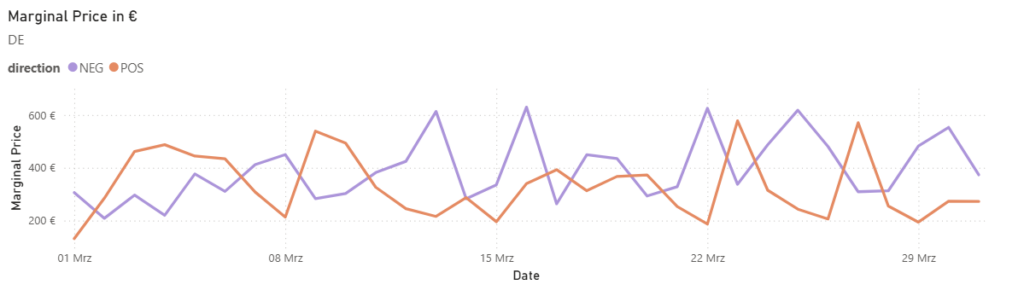

In March, the balancing capacity markets in Germany and Austria presented an exceptionally dynamic picture, characterized by a nearly widespread and massive increase in price levels. In both countries, marginal prices in the aFRR showed a clear upward trend, with the negative markets, in particular, recording an extreme surge. This trend also continued with great momentum in the mFRR- , while the positive markets developed more variably. Following the downward trends in February, the movement in the FCR also reversed significantly, marking a strong recovery in revenues in both markets.

In Austria, marginal prices in aFRR– rose massively from €2,066/MW/h in February to €10,434/MW/h in March. At the same time, aFRR+ also saw a significant increase from €4,738/MW/h to €7,719/MW/h.

Marginal prices in the mFRR followed suit with a sharp upward movement: mFRR– recorded a jump from €1,850/MW/h to €12,065/MW/h, while prices in mFRR+ increased from €3,167/MW/h to €4,692/MW/h.

In the FCR, the previous month’s trend also reversed, with revenues rising markedly to €13,230/MW/h after having stood at €6,959/MW/h in February.

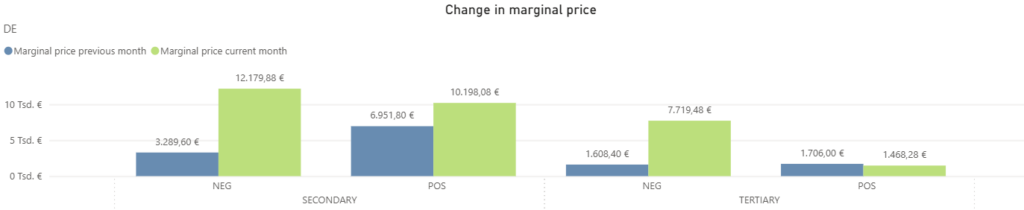

In Germany, March presented a consistently dynamic picture with a clear upward trend across almost all markets. In aFRR–, marginal prices rose massively from €3,290/MW/h in February to €12,180/MW/h in March. A clear increase was also recorded in aFRR+, which rose sharply to €10,198/MW/h after the decline in the previous month.

The mFRR followed this development with great momentum in the negative segment. In mFRR–, there was a significant increase in marginal prices from €1,608/MW/h to €7,719/MW/h. In contrast, mFRR+ continued its slight downward movement, falling from €1,706/MW/h in February to €1,468/MW/h in March.

The trend of the previous month was also reversed in the FCR market. After revenues had decreased in February, the FCR saw a striking increase in March, with revenues climbing from €5,778/MW/h to €12,343/MW/h.

Comparison of revenues generated with FPH and the market average in the aFRR

In March, the balancing capacity markets in Germany and Austria exhibited exceptional dynamics, leading to a massive increase in revenues across the secondary markets. This positive development was reflected in a significant rise in market averages, with FlexPowerHub efficiently capturing market trends through precise forecasting and further consolidating its performance relative to the market average in many segments. Consequently, significantly higher revenues were realized compared to both the previous month and the previous year.

Austria

In March, the revenues achieved with FlexPowerHub in aFRR+ recorded a significant increase of 161% to €5,314/MW/h, following €3,304/MW/h in February.During the same period, the market average also rose sharply from €3,569/MW/h to €5,701/MW/h (+60%), meaning that revenue development successfully mirrored the positive market movement. The bid acceptance rate decreased slightly to 90%, while the forecast performance remained stable at a high level of 93%.

An even more dynamic development was observed in aFRR–: here, revenues rose massively by 636% to €6,388/MW/h (previous month: €1,004/MW/h). Parallel to this, the market average climbed from €1,255/MW/h to €7,240/MW/h. The bid acceptance rate improved significantly to 92% from 86% in the previous month. Forecast performance also increased markedly from 80% in February to 88% in March.

Compared to March 2025, a significantly more stable performance is evident: while revenue development in aFRR– lagged behind the market in the previous year, FlexPowerHub was able to fully capitalize on the current market dynamics while simultaneously increasing the bid acceptance rate.

Germany

In the German aFRR+, revenues achieved with FlexPowerHub increased by 50% to €6,255/MW. The market average rose in parallel from €5,231/MW to €7,618/MW, meaning the trend continued to be strongly driven by the overall higher price level in aFRR+. The bid acceptance rate remained at a very high level, reaching 95% in March. During the same period, our forecast performance improved to 82%. A comparison with March 2025 shows a significantly more positive dynamic, as the market average nearly stagnated last year, whereas a strong increase was recorded this time.

In aFRR– revenues rose massively to €7,342/MW in March, up from €1,378/MW in the previous month. The market average followed this trend significantly, climbing from €1,829/MW to €8,771/MW. The bid acceptance rate showed a downward trend, moving from 82% in February to 73% in March. In contrast, forecast performance improved significantly, reaching 84% in March compared to 75% in the previous month. Compared to March 2025, the current growth is even more pronounced, highlighting the enormous volatility and increased revenue potential in the negative segment.

Market volatility

In March, the Austrian and German aFRR markets presented a striking picture, characterized by a significantly higher price level in both markets compared to the previous month. While February was still defined by a very low baseline with isolated, extreme spikes toward the end of the month, March exhibited much more constant and steady volatility. In the aFRR–, a consolidated, higher price level established itself, largely avoiding the jumps observed in the previous year. The aFRR+ also saw an increase in dynamics with more frequent fluctuations, which were nonetheless more stable than the isolated peaks of the preceding months. Overall, a market stabilization at a high price level can be observed, in which volatility increased but was less characterized by sharp outliers.

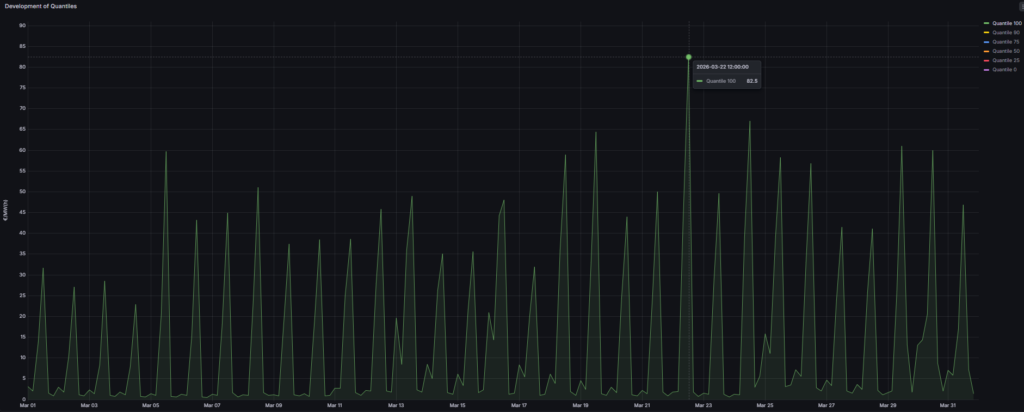

In the Austrian aFRR–, March was characterized by a significantly higher price level, defined by steady volatility. While prices in the first half of the month largely remained stable below 60 €/MW/h, the monthly high was reached on March 22 at 82.5 €/MW/h. Despite this nominally higher level compared to February 2026, market dynamics remained consistent and avoided isolated, extreme outliers. The fact that this market development was precisely anticipated is reflected in the forecast performance, which increased to 88%. Thanks to this high predictive quality, market opportunities were utilized efficiently, allowing the bid acceptance rate to be significantly improved to 92%.

A look at the year-on-year comparison underlines this homogeneity: while March 2025 was marked by erratic developments with peak values of up to 95 €/MW and drops to 4.39 €/MW, the current March showed a much more solidified structure. The market environment has thus stabilized on a higher price foundation but exhibits a significantly lower susceptibility to the price jumps observed in the previous year.

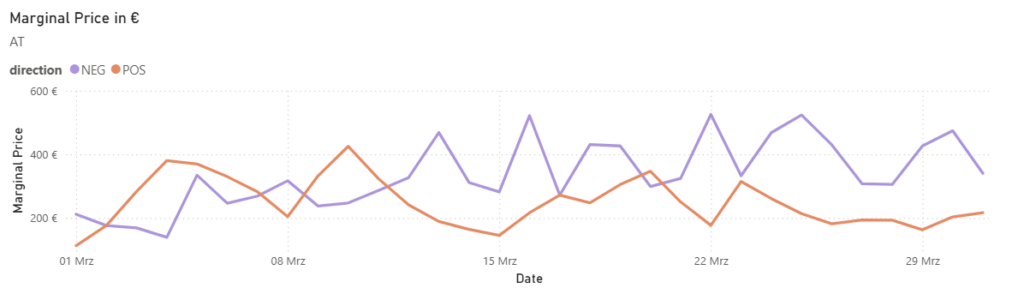

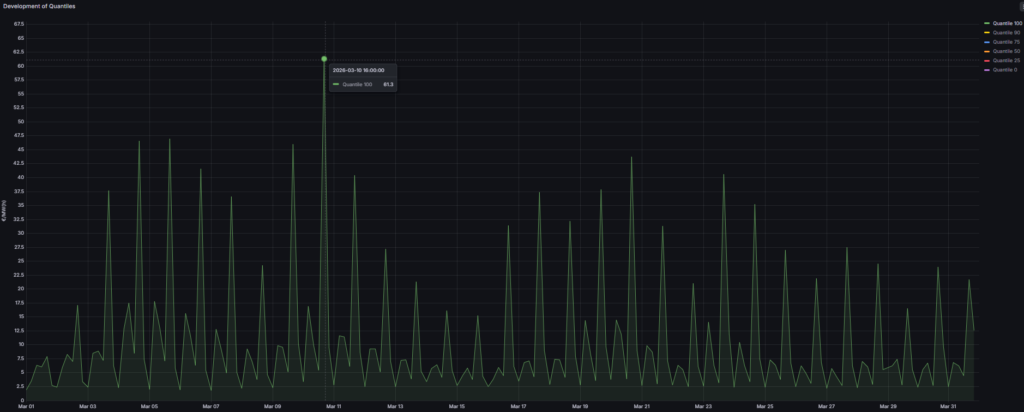

In the Austrian aFRR+, March exhibited a significantly more dynamic development compared to the previous month. After starting at a low level, prices rose to values above €35/MW/h within the first week. This upward trend culminated in a monthly high of €61.3/MW/h on March 10 at 4:00 PM, placing the March maximum well above the February peak of €39/MW/h. Following this peak, prices declined steadily toward the middle of the month to a level below €17.5/MW/h, before rising again in the second half of the month without any sharp outliers.

In this dynamic environment, our forecast performance remained stable at a high level of 93%, underlining the reliability of the models. The bid acceptance rate only slightly declined to 90%, which represents a very solid result given the significantly increased price volatility.

A comparison with March 2025 highlights the changed market characteristics: last year, prices remained stable below €26/MW/h for most of the month and were only marked by two distinct spikes on March 7 (€43.7/MW/h) and March 20 (€45.3/MW/h). While March 2025 was thus defined by occasional peaks within an otherwise flatter environment, the current month operated at an overall elevated price level with much more stable fluctuations.

In the German aFRR–, March 2026 was characterized by a significantly higher price level compared to February. While prices in the previous month remained at a calm baseline of under €10/MW/h for long periods, they moved within a range of under €55/MW/h for most of March. Despite this general upward shift, the market remained spared from extreme individual jumps. In particular, an extraordinary outlier like the one observed on February 25 at €97/MW/h did not occur in the current reporting month. The monthly high was reached on March 22 at €89.3/MW/h. This shift in the price structure was also reflected in the key performance indicators: while the forecast performance improved significantly to 84%, allowing the new market dynamics to be predicted more accurately, the bid acceptance rate showed a downward trend at 73%.

Compared to the previous year, a change in the market structure is evident: while March 2025 was defined by steady fluctuations without sharp outliers, price formation this year was more constant. The market environment has thus developed away from continuous wave-like movements toward a more stable, albeit overall higher, price dynamic.

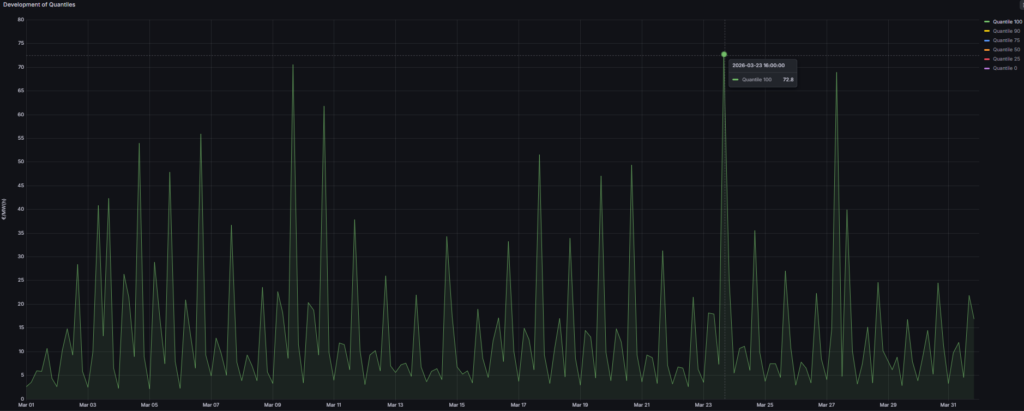

In the German aFRR+, March 2026 was characterized by a noticeable increase in dynamics and an overall higher price level than in the previous month. While the price pattern in February remained largely moderate (below €35/MW/h) and was only interrupted by occasional peaks up to a maximum of €55/MW/h, an environment with more frequent fluctuations established itself in March. These movements led to price levels regularly climbing above the €40 mark, with the monthly high of €72.8/MW/h recorded on March 23 at 4:00 PM. The fact that we were able to capitalize profitably on this volatility is demonstrated by the outstanding bid acceptance rate, which was stabilized at a very high level of 95% in March. This success was flanked by an improved forecast performance of 82%, proving that our models were able to accurately capture the more frequent price spikes.

A comparison with March 2025 highlights the shift in volatility structure: the previous year was characterized by prices below €40/MW/h for almost the entire month, interrupted only by occasional price spikes, with the extreme outlier of €372/MW/h on March 6 being the most prominent. In March 2026, however, such isolated, extreme price jumps did not occur. Instead, they were replaced by steady volatility with several regular fluctuations at an overall elevated level. The German market has thus evolved in March 2026 away from isolated individual events toward a more rhythmic and therefore more predictable price dynamic.

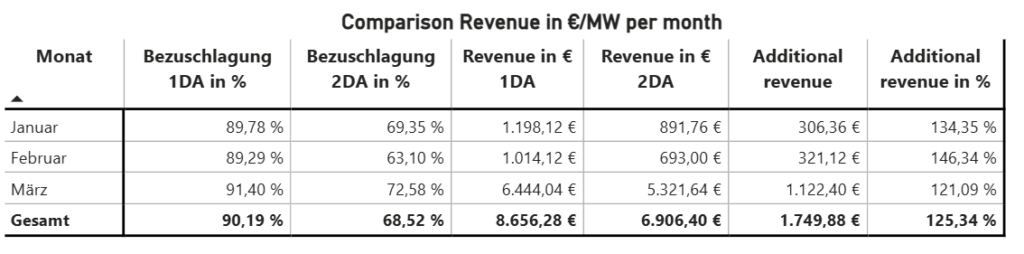

1DA vs. 2DA

In March 2026, the trend of outperformance by the 1-day-ahead forecast (1DA) compared to the 2-Day-Ahead forecast (2DA) continued across all analysed aFRR markets. In a market environment characterized by a significantly higher price level and stabilized volatility compared to February, the shorter forecast horizon in Austria and Germany again enabled an optimized bidding strategy and consequently significantly increased total revenues.

In Austria, the results underpinned the economic added value of the 1DA in both directions. In aFRR–, the 1DA bid acceptance rate rose to 91.4% in March, while the 2DA stood at 72.6%. This resulted in an additional revenue of €1,122/MW/m. The advantage also remained prominent in aFRR+. With an acceptance rate of 91.9%, the 1DA generated revenues of €5,297/MW/m, achieving an additional revenue of €1,032/MW/m.

The German market reflected this positive development with similarly sharp increases in absolute values. In aFRR–, the 1DA reached a bid acceptance rate of 93.6%, while the 2DA was only 73.7%. In terms of revenue, this led to €6,890/MW/m for the 1DA compared to €5,936/MW/m for the 2DA. In aFRR+, the lead of the 1DA was also clearly pronounced. Despite a slightly smaller difference in the bid acceptance rate, the 1DA achieved a high additional revenue of €1,089/MW/m with total revenues of €5,960/MW/m.

In summary, March 2026 illustrates that the 1-day-ahead forecast provides a consistent advantage in both countries and directions. Especially given the massive price increase observed this month, the short-term adaptability of the 1DA paid off through more efficient market participation and noticeably higher revenues.