Revenues and marginal prices — an overview covering all markets

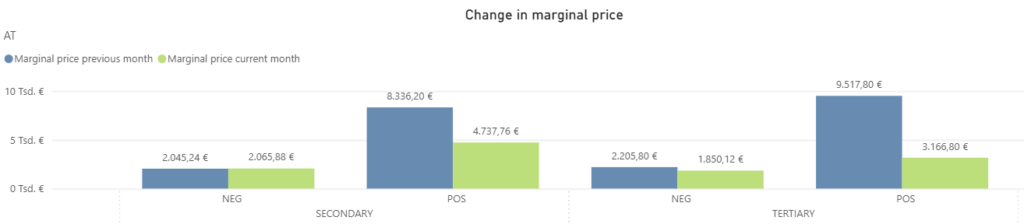

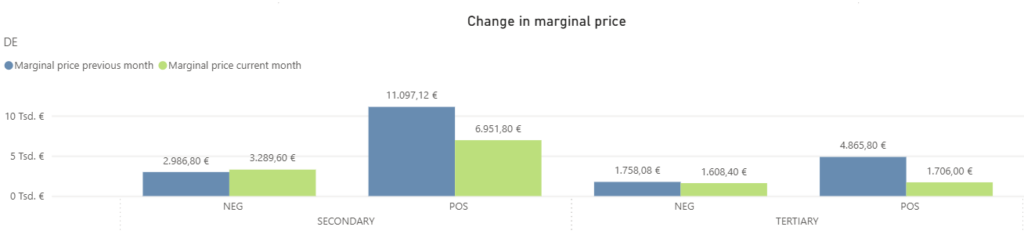

In February, the overall price level in the balancing capacity markets in Germany and Austria remained moderate, but developments were more differentiated than in the previous month. In the aFRR, marginal prices moved in opposite directions: while aFRR– increased slightly in both countries, aFRR+ declined markedly. The mFRR also weakened, with a particularly strong correction in mFRR+. After the high January levels, FCR also moved lower.

In Austria, aFRR– marginal prices rose slightly from 2.045 €/MW/h in January to 2.066 €/MW/h in February. At the same time, the aFRR+ fell significantly from 8.336 €/MW/h to 4.738 €/MW/h. In the mFRR, marginal prices moved lower overall: mFRR– decreased from 2.206 €/MW/h to 1.850 €/MW/h, while mFRR+ dropped sharply from 9.518 €/MW/h to 3.167 €/MW/h. The FCR revenues also declined, falling from 9.625 €/MW/h in January to 6.959 €/MW/h in February.

Germany showed a very similar pattern. In the aFRR–, marginal prices increased from 2.987 €/MW/h in January to 3.290 €/MW/h in February, while aFRR+ fell from 11.097 €/MW/h to 6.952 €/MW/h. The mFRR also trended downward: mFRR– eased slightly from 1.758 €/MW/h to 1.608 €/MW/h, while mFRR+ dropped more strongly from 4.866 €/MW/h to 1.706 €/MW/h. The FCR also softened, with marginal prices declining from 7.945 €/MW/h to 5.778 €/MW/h.

Comparison of revenues generated with FPH and the market average in the aFRR

In February, the aFRR market environment in Austria and Germany remained overall moderate, while still showing clear differences between directions. In aFRR+, both the revenues achieved with FlexPowerHub and the market average declined noticeably in both countries, whereas movements in aFRR– were clearly more moderate.

Austria

In the Austrian aFRR+, revenues achieved with FlexPowerHub fell sharply by 43% to 3.304 €/MW/h in February, after reaching 5.000 €/MW/h in the previous month.

The market average also declined significantly over the same period, from 6.075 €/MW/h to 3.569 €/MW/h (-41%), meaning our revenue development was clearly in line with the market move. At the same time, the bid acceptance rate increased by 7% to 92%, after 86% in the previous month. Our forecast performance also improved markedly, rising from 82% in January to 93% in February.

In the aFRR–, revenues decreased to 1.004 €/MW/h from 1.313 €/MW/h in the previous month. The market average also eased slightly, falling from 1.337 €/MW/h to 1.255 €/MW/h. In February, the bid acceptance rate at 86% was slightly below the January level of 89%, while forecast performance dropped noticeably from 98% to 80%.

Germany

In the German aFRR+, revenues achieved with FlexPowerHub decreased by 28% to 4.173 €/MW/h in February, compared to 5.821 €/MW/h in January. The market average fell in parallel from 7.763 €/MW/h to 5.231 €/MW/h, meaning the move continued to be driven by the overall weaker price level in aFRR+. The bid acceptance rate remained high at 94%. Over the same period, our forecast performance improved to 80% from 75% in January.

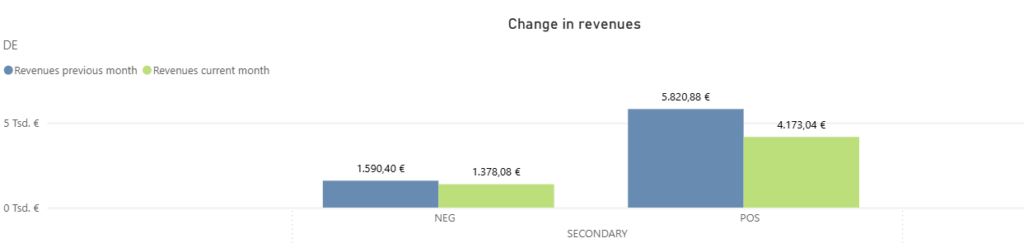

In the aFRR–, revenues decreased slightly to 1.378 €/MW/h from 1.590 €/MW/h in the previous month. The market average followed this development, declining from 2.064 €/MW/h to 1.829 €/MW/h. The bid acceptance rate fell to 82% from 87% in January. Forecast performance remained broadly stable at 75% compared to 77% in the previous month.

Market volatility

In February, the aFRR in Austria and Germany showed a very similar movement pattern in both directions, even though price levels differed. In the aFRR–, the baseline remained low for most of the month before volatility increased noticeably in the second half, with several stronger swings clearly visible toward month end. The aFRR+ was characterised by continuous fluctuations. Overall, this results in a consistent cross-country picture, with aFRR– gaining momentum over the course of the month, while aFRR+ fluctuated throughout but without equally pronounced price spikes.

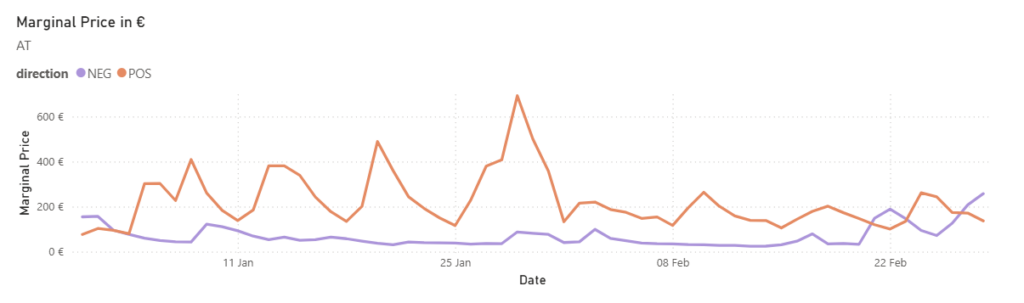

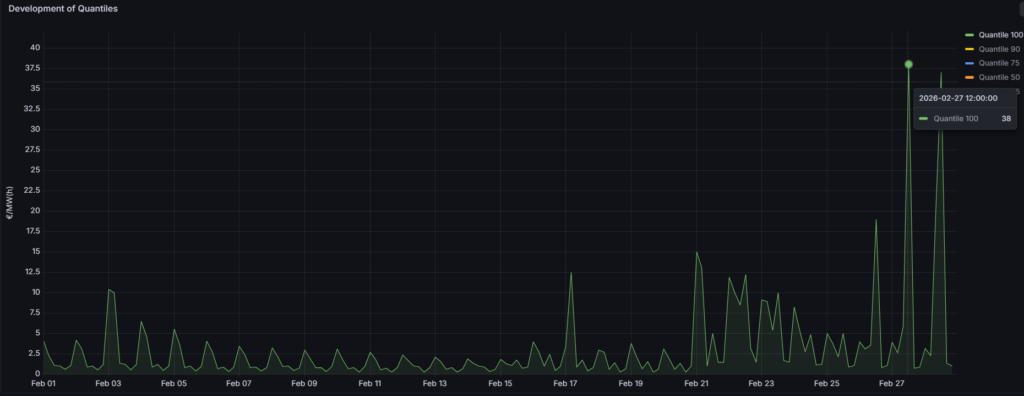

In the Austrian aFRR–, February remained at a low and stable price level for most of the month. In most MTUs, prices stayed below 10 €/MW/h, reflecting a generally calm market environment. Following a spike on 21 February to 15 €/MW/h, volatility increased, with several stronger moves toward the end of the month. The most pronounced move occurred on 27 February, when the price briefly rose to 38 €/MW/h, marking the monthly high.

Compared to January, when the monthly high was 21 €/MW/h, February was therefore more volatile, with the strong late month price spikes not observed in January. In this environment, the bid acceptance rate remained relatively stable at 86% compared with 89% in January. Our forecast performance declined, but at 80% it remained at a good level.

In the aFRR+, the price level fluctuated for most of the month at a moderate level below 20 €/MW/h. A first, still moderate, swing was seen on 10 February at 16:00, when the price briefly rose to around 26 €/MW/h. The most pronounced move followed on 24 February, when the price increased within four hours from 4 €/MW/h to the monthly high of 39 €/MW/h and then stepped down again. Further fluctuations were observed until the end of the month, but these were overall less pronounced than in January, which was characterised by recurring stronger spikes and reached a monthly high of 56 €/MW/h.

The bid acceptance rate increased to around 92% from around 86% in the previous month. Forecast performance also improved noticeably, reaching 93% compared with 82% in January, suggesting that February’s price movements were overall more consistent to forecast.

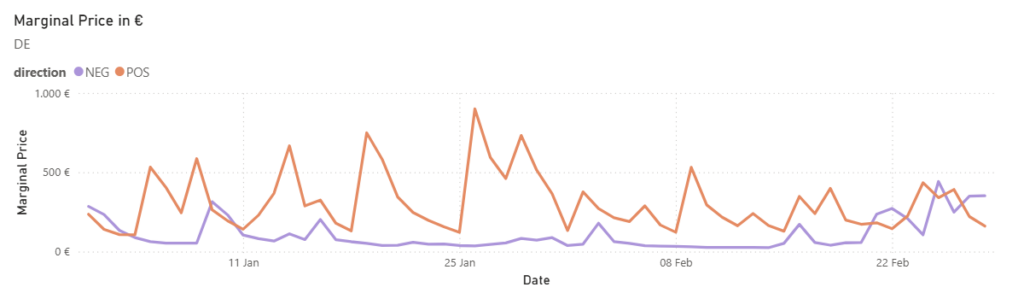

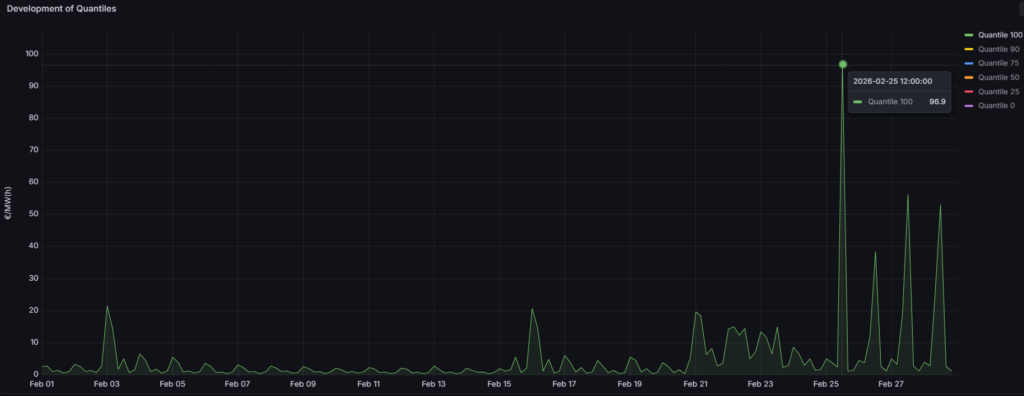

In the German aFRR–, February remained at a low price level for most of the month, similar to Austria, with the baseline staying below 10 €/MW/h in many MTUs. This pattern was only occasionally interrupted by spikes to around 21 €/MW/h. A particularly striking event occurred on 25 February, when the price rose within four hours from 2 €/MW/h to 97 €/MW/h, marking the monthly high.

This also shows a clustering of stronger late month moves in Germany, analogous to the pattern in Austrian aFRR–, but with a significantly higher extreme value. Im Vergleich zum Januar, der in diesem Segment zwar Peaks zeigte, aber mit einem Monatshoch von 46 €/MW/h deutlich darunter blieb, war der Februar damit klar extremer.

At 82%, the bid acceptance rate was below the January level of 87%. Forecast performance remained nearly stable at 75% compared with 77%, indicating that our model continued to capture the underlying trend well, despite the sharp spike and higher prices toward month end.

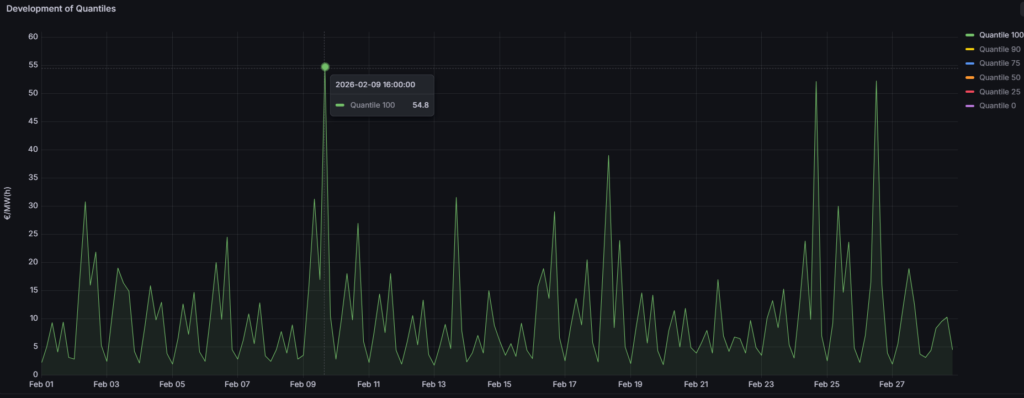

In the German aFRR+, the baseline in February was moderate across many time slices, showing a similar underlying pattern to Austria. In Germany, however, this calmer picture was interrupted by a few clearly defined price spikes. The strongest move occurred on 9 February, when the price briefly rose to 55 €/MW/h, marking the monthly high.

Compared to January, February was noticeably less pronounced, as the recurring strong spikes into the range above 70 €/MW/h did not occur. At 94%, the bid acceptance rate remained high, but was below the previous month’s 96%. Forecast performance increased to 80%, suggesting that market movements in February were overall more predictable than in January.

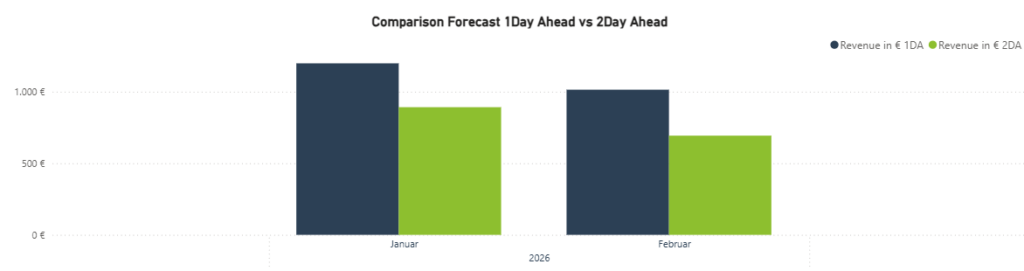

1DA vs. 2DA

February 2026 once again showed a clear advantage of the 1-day-ahead forecast over the 2-day-ahead forecast in the aFRR markets. In both Austria and Germany, the shorter forecast horizon again led to higher bid acceptance rates and, as a result, to noticeable revenue uplifts. Compared to January, the relative edge of the 1DA broadly remained in place, even though absolute revenues in both directions were lower due to the overall weaker price environment.

In Austria, the added value of the 1DA was confirmed in both directions. In aFRR–, the bid acceptance rate in February, at 89%, was close to January levels, while the 2DA at 63% remained clearly lower. As a result, the 1DA generated revenues of 1.014 €/MW/m versus 693 €/MW/m for the 2DA, corresponding to an additional revenue of 321 €/MW/m and thus slightly above the January uplift. In aFRR+, the advantage also remained clearly visible, even though absolute revenues declined compared to January. The 1DA achieved a bid acceptance rate of 94% versus 69% and generated 3.304 €/MW/m, corresponding to an uplift of 716 €/MW/m.

Germany showed the same pattern in February, with the 1DA outperforming the 2DA in both directions. In aFRR–, the 1DA achieved a bid acceptance rate of 89% versus 75% for the 2DA and generated 1.354 €/MW/m compared to 903 €/MW/m, resulting in an additional revenue of 452 €/MW/m. For the aFRR+, the advantage was even more pronounced, as the 1DA reached 89% bid acceptance versus 67% for the 2DA and delivered 3.965 €/MW/m, corresponding to an uplift of 1.030 €/MW/m. This made the German aFRR+ segment the largest absolute 1DA uplift among all segments considered in February.

Overall, February once again confirms that the 1-day-ahead forecast delivers a clear advantage over the 2-day-ahead forecast in both countries and in both directions. Especially in a market environment that was calm for long stretches but became noticeably more volatile toward month end, the superior short-term adaptability of the 1DA paid off again in February.