Revenues and marginal prices — an overview covering all markets

The balancing capacity markets in Germany and Austria presented a differentiated picture which deviated significantly from the parallel upward trend of the previous year. While Austria recorded a continuation of price increases across all market segments the high price level in the German aFRR cooled down noticeably. In the tertiary balancing capacity market German marginal prices moved in opposite directions. In parallel the FCR continued its upward trend in both countries with moderate revenue increases.

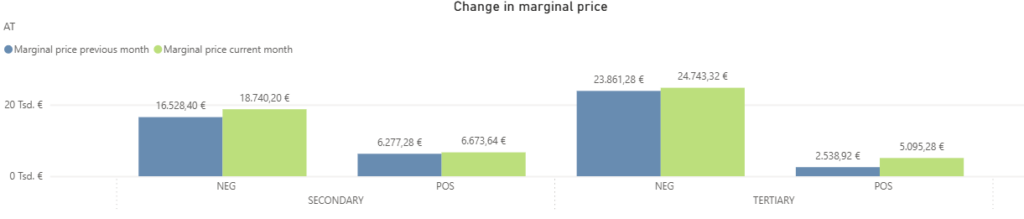

In Austria, an exciting trend reversal emerged in May, which led to an overall positive development of marginal prices across all segments. After the aFRR+ had noticeably declined in April, this segment recovered in May and recorded an increase of 6% to 6,674 €/MW/h. In the aFRR-, the upward movement continued so that the values climbed by around 13% from 16,528 €/MW/h to 18,740 €/MW/h. These widespread increases in the secondary balancing capacity market correspond to the picture from May of the previous year in which price increases were also observed.

The mFRR+ presented an even more striking countermovement. After the downward trend of the previous month, marginal prices literally doubled here and recorded a massive growth of over 100% to 5,095 €/MW/h. The mFRR- also grew and increased by nearly 4% from 23,861 €/MW/h to 24,743 €/MW/h. However, this development was significantly more moderate than in April, when the segment literally exploded and prices almost doubled. At the same time, this slight growth in May 2026 marks an interesting difference to the previous year since the Austrian mFRR- was the only market to experience a price drop in May 2025. The FCR once again developed very pleasingly and consistently with revenues increasing by around 6% from 17,080 €/MW/h to 18,086 €/MW/h.

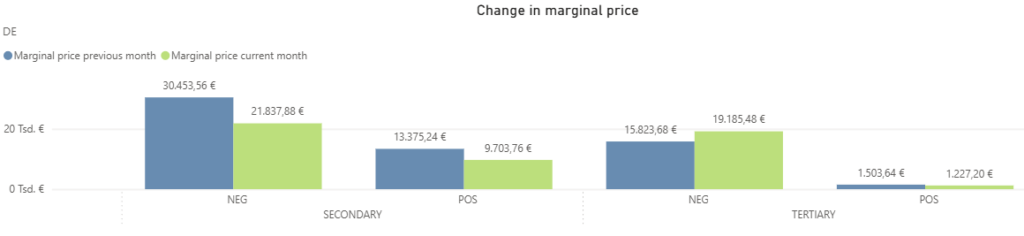

In Germany, an entirely different picture presented itself, which stood in strong contrast to the ongoing dynamics in Austria as well as to the widespread upward movement of the same month last year. After the massive price increases in April, marginal prices in the aFRR recorded a clear downward correction. In the aFRR-, values fell noticeably by 28% from 30,454 €/MW/h to 21,838 €/MW/h. Analogously, the aFRR+ also declined significantly and sank by 27% from 13,375 €/MW/h to 9,704 €/MW/h.

In the mFRR, a directionally divergent development was evident. The mFRR- continued its strong growth and increased by 21% from 15,824 €/MW/h to 19,185 €/MW/h. With this, the segment confirmed its role as the strongest growth driver exactly as in May 2025. In the mFRR+, however, a clear trend reversal was apparent. After marginal prices had remained absolutely stable and even slightly increased in April, they now noticeably declined in May and sank by 18% from 1,504 €/MW/h to 1,227 €/MW/h. This countermovement also marks a clear difference to the previous year, since widespread price increases were recorded across the entire mFRR in May 2025. The FCR joined the positive development of the neighbouring country and recorded a moderate revenue increase of almost 5% from 16,523 €/MW/h to 17,269 €/MW/h.

Comparison of revenues generated with FPH and the market average in the aFRR

In May, the balancing capacity markets in Germany and Austria recorded a continued dynamic development which led to a strong increase in revenues, particularly in the negative segments. FlexPowerHub managed in an impressive manner to efficiently capture the available revenue potential through precise forecasting. Our excellent operational performance is particularly in focus here as we were able to massively increase bid acceptance rates in almost all segments and thus positioned ourselves much more positively than in the same month last year.

Austria

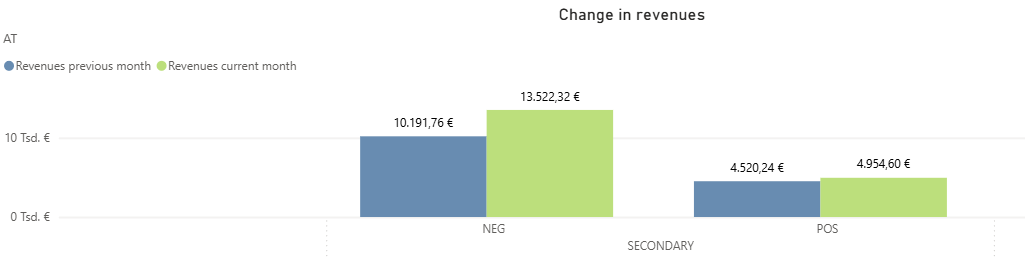

In the aFRR+, revenues achieved with FlexPowerHub recorded a pleasing increase of almost 10% from 4,520 €/MW/h to 4,955 €/MW/h in May. The market average climbed somewhat more moderately over the same period by a good 6% from 4,743 €/MW/h to 5,041 €/MW/h which means FlexPowerHub successfully outperformed the general market growth. Our bid acceptance rate remained at an excellent and almost unchanged level of 93%. At the same time our forecast performance made a remarkable leap from around 95% to an outstanding 98%. This circumstance is particularly interesting compared to the previous year. In May 2025, we also recorded a strong revenue growth but had to accept a 10% decline in the bid acceptance rate. In May 2026, however, we succeeded in combining rising revenues with maximum placement reliability.

The picture in the aFRR- was once again even more dynamic.. Here, the revenues achieved with FlexPowerHub noticeably increased by almost 33% and rose from 10,192 €/MW/h in April to a strong 13,522 €/MW/h. The market average grew in parallel by around 21% from 12,039 €/MW/h to 14,554 €/MW/h. Here too our percentage revenue development clearly exceeded the market growth. This success was accompanied by an increased bid acceptance rate which climbed from 91% to an excellent 95%. In addition the forecast performance improved massively from just under 85% to 93%. This development marks an extremely strong contrast to the previous year. Although our revenues in May 2025 were at a similar absolute level of 14,138 €/MW/h the bid acceptance rate dropped significantly by 14% at that time. In the current reporting month however we leveraged the market dynamics highly efficiently and placed the bids confidently.

Germany

In the German aFRR+ a slightly different picture emerged. Here revenues generated with FlexPowerHub minimally declined by around 1% from 6,053 €/MW/h to 5,979 €/MW/h. In the context of the general market dynamics this result underlines our high performance since the market average declined by a good 9% at the same time. FlexPowerHub was thus able to almost completely cushion the general market downturn. A key driver for this was our outstanding bid acceptance rate which shot up from 88% in April to an excellent 96%. Forecast performance also noticeably increased from a good 75% to 82%. This market phase differs fundamentally from the previous year. In May 2025 the aFRR+ still experienced a clear revenue growth which however was accompanied by declining bid acceptance rates. In the current year our models secured an outstanding market coverage even with slightly falling prices.

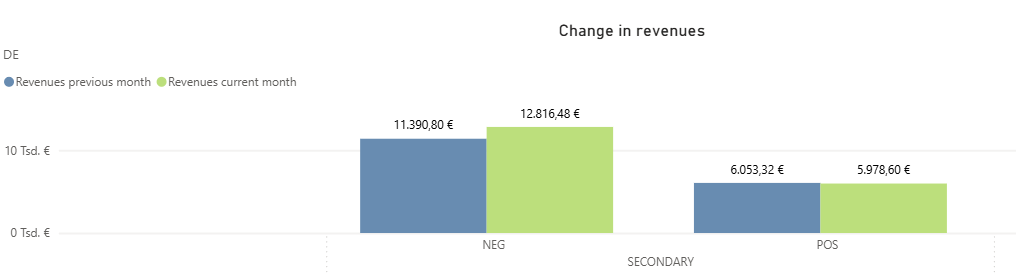

In perfect alignment with the Austrian market the aFRR- recorded strong revenue growth. Revenues achieved with FlexPowerHub climbed by a good 12% from 11,391 €/MW/h to 12,816 €/MW/h. The market average followed this upward movement with an increase of almost 16% from 14,735 €/MW/h to 17,043 €/MW/h. Our operational performance is once again highly remarkable in this environment. The bid acceptance rate improved massively and rose from 86% in April to a brilliant 96%. With this we excellently captured the market potential despite the high dynamics. Forecast performance leveled off at a solid 75%. The direct comparison to May 2025 additionally illustrates our enormously increased placement reliability. While our bid acceptance rate in the same month last year was still at a comparatively low 66% we were able to massively increase this value to 96% in the current reporting month. Our models thus navigated confidently through the current market growth and guaranteed our customers absolutely reliable market access.

Market volatility

In May, market volatility in the secondary balancing capacity markets in Austria and Germany was noticeably calmer than in the previous month. The extreme isolated events and gigantic price spikes which had characterized the German market in April were completely absent in May. Instead, a rhythm of continuous fluctuations established itself at a much more moderate extreme level. A look at May 2025 also reveals a strong contrast, since massive outliers were still observed in both countries in the previous year. Our operational key figures impressively demonstrate that FlexPowerHub precisely anticipated these more stable market dynamics and confidently translated them into excellent economic success.

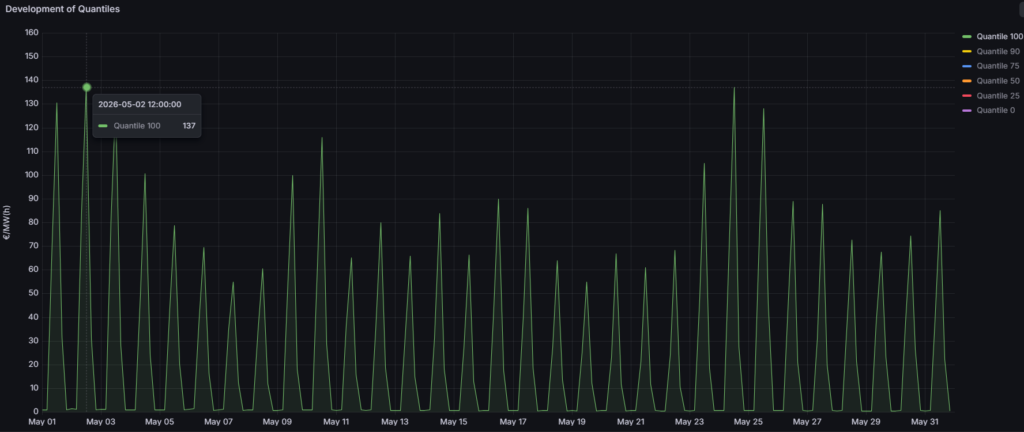

In the Austrian aFRR- May was characterized by a continued and rhythmic dynamic which strongly resembled the pattern of the previous month. The monthly high was reached twice. Both on 2 May at 12:00 and on 24 May at 12:00, prices climbed to a peak value of 137 €/MW/h. This corresponds almost exactly to the peak value from April, which was 133 €/MW/h. A remarkable stability is also evident in the year-on-year comparison, since prices in May 2025 also moved in an almost identical range of up to 135 €/MW/h. In this familiar environment, our forecast models proved their enormous strength. Forecast performance shot up from just under 85% in April to an excellent 93% in May. This brilliant forecasting quality was accompanied by a massively increased bid acceptance rate, which climbed from around 91% to an outstanding 95%. These values highlight that FlexPowerHub optimizes market access highly efficiently and fully captures the available potentials.

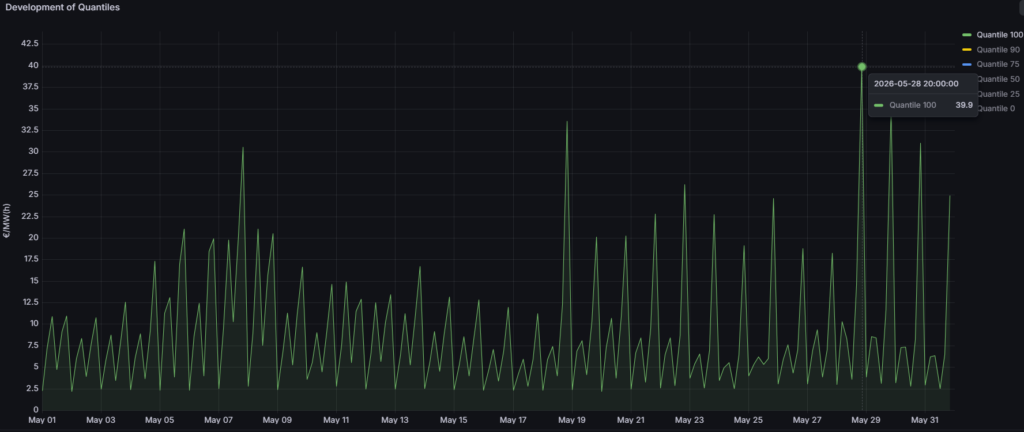

The aFRR+ showed a quite lively but overall very well predictable market dynamic which exhibited continuous fluctuations over the course of the month. While prices moved in a corridor of below 30 €/MW/h for long stretches and showed regular fluctuations, a first prominent peak of 33.6 €/MW/h occurred on 18 May. Towards the end of the month, the development then intensified somewhat again. The absolute monthly high was reached on 28 May at 20:00 with just under 40 €/MW/h. In direct comparison to the previous month in which the maximum was 33 €/MW/h this marks a slight increase in peak fluctuations. The comparison to the previous year, however, reveals an entirely different picture. In May 2025, a massive price spike of 121 €/MW/h still occurred in this segment. May 2026 was thus significantly flatter and more predictable here. Our algorithms leveraged this reliable market phase in an impressive manner. The already high forecast performance could be increased once again and reached an almost perfect 98%. In parallel, the bid acceptance rate levelled off at a very solid 93% which once again underpins our consistently high placement reliability.

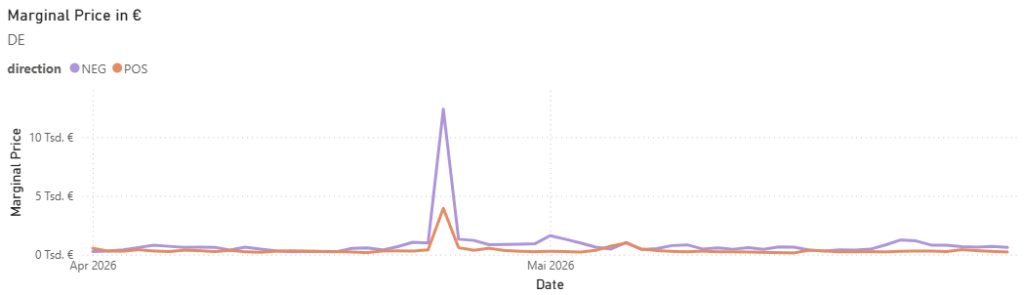

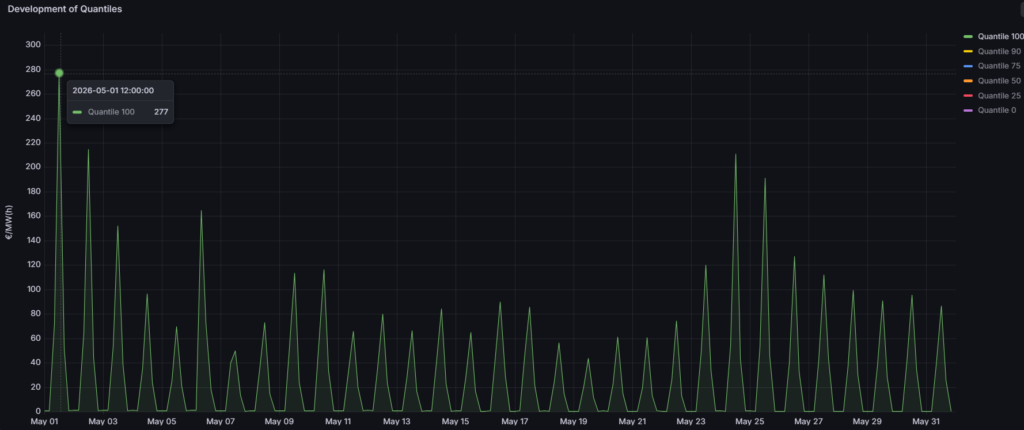

In the German aFRR- a massive trend reversal took place in May regarding peak values. While April was still dominated by an unprecedented extreme event of over 2,000 €/MW/h the market returned to a much more moderate volatility in May. The absolute high was recorded on 1 May at 12:00 with 277 €/MW/h. This value not only marks a massive cooling compared to the previous month but also an enormous contrast to May 2025 in which a gigantic spike of 1,597 €/MW/h still characterized the market activity. Despite this abrupt return to a noticeably calmer environment FlexPowerHub mastered the challenge excellently. The bid acceptance rate improved massively from 86% in April to a brilliant 96% in May. Forecast performance leveled off at a solid 75%. These figures impressively prove that our models consistently and confidently master the balance between risk and revenue maximization.

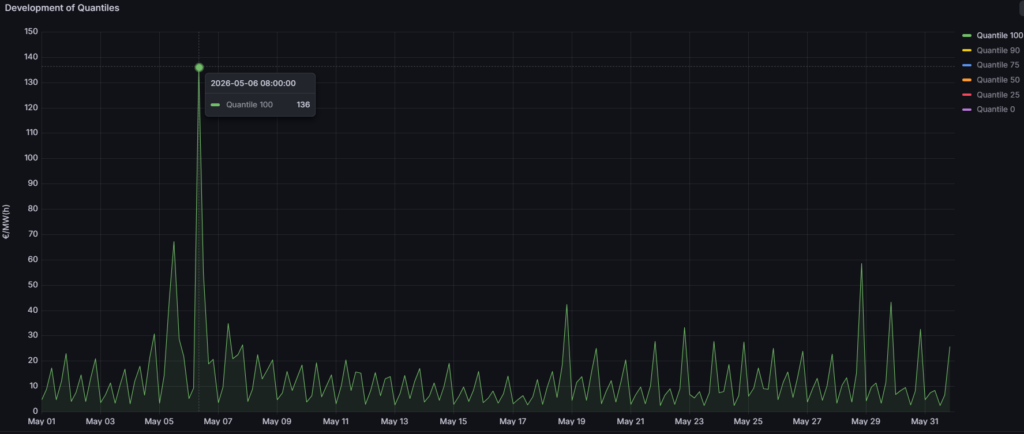

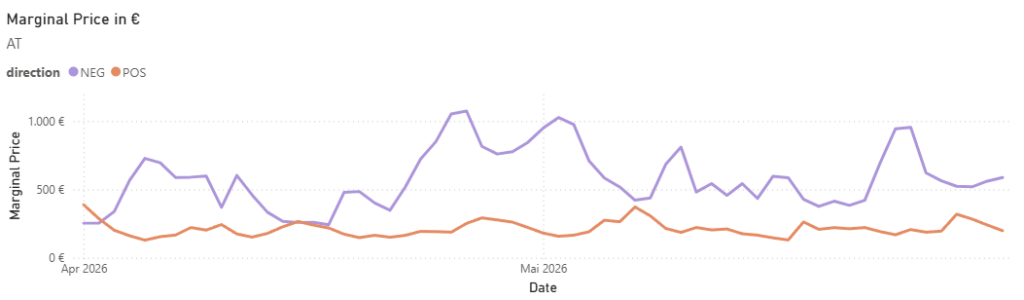

In the aFRR+ a significantly calmer market picture presented itself in May compared to the previous months. Also in direct connection with the clear market cooling in the negative segment, a well predictable dynamic returned here. The absolute monthly high was recorded on 6 May at 08:00 with 136 €/MW/h. Apart from this isolated spike, however, prices moved at a very stable level of below 50 €/MW/h for the majority of the month, which was only interrupted by a few smaller outliers. Analogous to the development in the aFRR- this represents a striking decline compared to the extremes of the previous month, in which peaks of 405 €/MW/h were still reached. The comparison to May of the previous year, which was characterized by a massive spike to 533 €/MW/h, also illustrates the significantly calmer market situation in the current reporting month. Such a changed market environment requires an extremely robust strategy. Our models delivered across the board here. Forecast performance noticeably improved from around 75% in April to a strong 82% in May. This success was flanked by an outstanding bid acceptance rate of 96% which represents a huge leap compared to the 88% of the previous month. FlexPowerHub thus guaranteed excellent market coverage even in this market phase.